Tax Day has come and gone, but while tax season isn’t on most people’s list of “favorite day of the year”, there’s a light at the end of the tunnel: your tax refund! The average refund in 2023 was $2,753, and with that kind of windfall, a tropical getaway might seem tempting. But before you jump on a plane, let’s explore how you can leverage your tax refund. A down payment for a first-time homebuyer, or long-term goals like financial freedom and building generational wealth!

Can I Use my Tax Refund for a Down Payment?

Are you dreaming of homeownership? Using your tax refund for a home purchase could lead to several advantages when owning your first home! Here are some benefits to a larger down payment on your loan:

Lower Interest Rate: A larger down payment can qualify a first-time homebuyer for a more favorable interest rate on your mortgage.

Smoother Pre-Approval Process: A bigger down payment strengthens your financial standing, with less “risk” for a lender to consider, this can make the pre-approval process smoother.

Avoiding PMI: With a down payment of at least 20% of the home’s value, you will avoid private mortgage insurance (PMI), which adds to your monthly mortgage payment.

Lower monthly payment: This one might be a no-brainer, but a larger down payment means a smaller loan amount. Smaller loan amount equals smaller monthly payment!

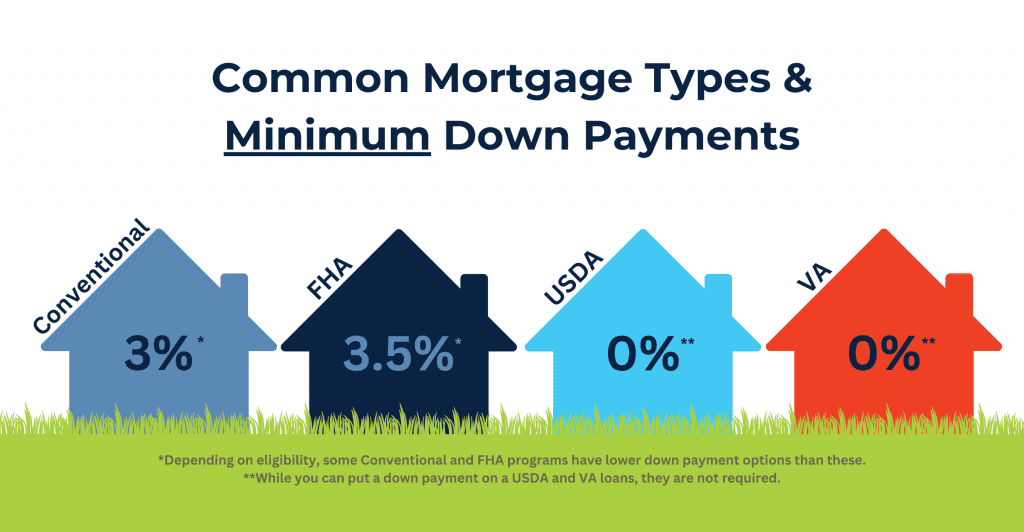

How Much do I Need for a Down Payment on my First Home?

Down payment requirements vary by the type of loan you want to have. Lower down payment doesn’t always mean a better loan program; there are multiple different factors to decide which loan program is right for you. The best mortgage for a first-time homebuyer is the loan that you’re most qualified for. That will depend on several factors, including your debt-to-income ratio, credit score, and yes…down payment.

We take all of these factors into consideration and help you strategize between your options and choose the right one to fit your current and future goals.

Mortgage Types and Minimum Down Payments

Related: Check out our mortgage calculators to do the down payment math yourself!

It’s easy to see how a first-time homebuyer can use a tax refund for a down payment and boost their homebuying strategy, but what about people that already own a home? Other than using the funds for home renovations, how can you use your refund to set yourself up for a better future?

Can I Pay Down Principal or Refi with a Tax refund?

We understand the allure of a vacation, but here’s the thing: by putting your tax refund towards your mortgage, you’re essentially doing two things at once: saving money on interest payments in the long run and building equity in your home faster.

Your tax refund may also be able to help you pay fees associated with refinancing to save you money by:

Lowering your interest rate

Shortening your loan term (from 30yr to 15yr)

Removing private mortgage insurance (PMI) that may have been required if your down payment wasn’t 20% or more of the cost of your home.

If you’ve decided to use your tax refund on your existing mortgage, there are a few ways to go about it:

1. Applying Tax Refund to Principal

A lump-sum payment directly to your principal balance, shortens your loan term, builds equity, and ultimately saves you on interest. The more you pay down the principal, the more interest you save.

Keep in mind:

Ensure the payment goes towards your principal, not just a regular payment (principal + interest).

Check for prepayment penalties – some mortgages have them for early large payments. Review your loan terms and talk to your lender if needed.

Some lenders might offer “loan recasting,” which recalculates your remaining loan term with the lower principal balance, potentially reducing your monthly payments.

If you’re looking for options to lower your monthly payments specifically, refinancing might be a good fit if rates have lowered since you first bought your home.

2. Using a Tax Refund for Refinancing Fees

Refinancing your mortgage means replacing your existing loan with a new one, potentially with a lower interest rate, better terms, or you could take cash out for projects or major life changes. Here’s where your tax refund can come in handy – it can help cover the refinancing fees, including closing costs and appraisals.

Is refinancing a good option for me?

Lower Interest Rates: Perhaps interest rates have dropped since you first took out your mortgage, offering an opportunity to save.

Improved Credit Score: If your credit score has improved significantly since the last time you bought a home, you might qualify for a lower interest rate.

Debt Reduction: Have you paid off other debts since buying your home? A lower debt-to-income ratio can improve your eligibility for a better interest rate.

While refinancing can save you money in the long run, there are upfront costs involved that you should consider. The Mortgage Reports estimates closing costs to range between 2-6% of your loan amount.

Here are some situations where refinancing might not be the best move for you:

Recently Closed Loan: Many lenders and loan programs have restrictions on how soon you can refinance after taking out a new mortgage. For almost everyone, you’ll want to wait 180 days before refinancing after your most recent loan began.

Minimal Interest Rate Drop: Aim for a rate reduction of at least 1.5-2% to make the refinancing process worthwhile compared to the cost.

Short-Term Ownership: If you plan to sell your home soon, refinancing might not make financial sense.

Longer Loan Term: Since a refinance is a new loan on the same property, you’ll be starting your loan term over again. A longer loan term might seem appealing for lower monthly payments, but it ultimately means paying more interest overall.

Not sure if refinancing is right for you? That’s why we’re here! Our team can do a complete cost analysis for you before you start the process, making sure you’re confident in your decision before taking the first step.

Boost Next Year’s Tax Refund

Let’s say your tax refund this year wasn’t quite enough to make a huge dent on your homeownership goals today. Don’t worry, there are still ways to optimize your tax situation for next year’s return, potentially putting more money back in your pocket to fuel your homeownership dreams.

Here are some key strategies to consider:

Tax Credits for Homeowners

Mortgage Credit Certificates (MCCs): These state-issued tax credits can be a game-changer, allowing you to claim a portion of your annual mortgage interest as a federal tax credit, effectively lowering your monthly payments.

Reach out to us to learn more about MCCs and eligibility requirements in your area!

Homeownership Tax Deductions

Mortgage Interest: You can typically deduct your mortgage interest payments, up to a certain limit depending on your loan amount and filing status.

Mortgage Points: If you paid upfront points to lower your interest rate, you might be able to deduct them as well, subject to specific IRS qualifications.

Property Taxes:The property taxes you pay on your home are generally deductible. If you dedicate a specific space in your home exclusively for work purposes, you might be eligible to deduct a portion of your related expenses like utilities and internet.

Home Office Expenses:If you dedicate a specific space in your home exclusively for work purposes, you might be eligible to deduct a portion of your related expenses like utilities and internet.

Keeping good records of your mortgage-related expenses is crucial. This includes your loan documents, receipts for points paid, and documentation of any home improvements you make.

It’s important to note that tax laws can be complex, and eligibility for deductions and credits can vary depending on your specific circumstances. Consulting with a tax professional is always recommended to ensure you’re taking advantage of all the benefits available to you and remaining compliant with federal tax law. We can help you explore these options, or get you in contact with a great Tax Advisor.

In Conclusion

By implementing these strategies and working with a trusted loan officer, you can turn your tax refund into a springboard for achieving your homeownership dreams. We’re here to guide you through every step of the journey, from maximizing your tax refund to navigating the mortgage process.

Get a no-cost pre-approval and explore down payment options for first-time homebuyers – click the Apply Now button above!

* NFM Lending is not a Financial Advisor, Tax Advisor or Credit Repair Company. You should consult with a Financial Advisor, Tax Advisor or Credit Repair Company to learn more. The pre-approval may be issued before or after a home is found. A pre-approval is an initial verification that the buyer has the income and assets to afford a home up to a certain amount. This means we have pulled credit, collected documents, verified assets, submitted the file to processing and underwriting, ordered verification of rent and employment, completed an analysis of credit, debt ratio and assets, and issued the pre-approval. The pre-approval is contingent upon no changes to financials and property approval/appraisal.

If you’ve been eyeing interest rates and waiting for an opportunity to refinance, your time has come! Refinancing is an excellent way to make your home work for you, and we’re answering the top five questions people have about refinancing.

How does refinancing work?

Refinancing is when your original loan is replaced with a new loan with different terms. It can be a smart move if you plan to stay in your home for a while; use a refinance mortgage calculator and speak with a lender to know your breakeven point. Many people refinance to lower their monthly payment, but it can also be used to access home equity, remove someone from the mortgage, get rid of private mortgage insurance (PMI), or change your loan type. Work with a loan originator to find out what refinance option is right for your needs.

What kinds of refinances are there?

Much like purchase loans, there’s no one-size-fits-all refinance. There are several types of refinances that can help you achieve your financial goals:

Rate and term refinance: This is the most common type of refinance because it allows you to lower your monthly payment or shorten the loan’s term. When interest rates drop, it’s a great time to take advantage of a rate and term refi, especially if you bought your home at a higher rate. You can also use this type of refinance to change your loan type (like going from an adjustable-rate to a fixed-rate mortgage) or remove PMI. Be aware that lowering your payment can lead to a longer term and more payments for the life of the loan, while choosing to shorten the repayment period can lead to a higher monthly payment.

Cash-out refi: A cash-out refinance leverages your existing home equity by replacing your first loan with a higher mortgage and giving you the difference in cash. There’s no limit to how you can use your newfound funds—they can be used to pay off debt, make home repairs, take a vacation, or to pay for tuition. Since a cash-out refinance is riskier, the rates can be slightly higher than other refinance types. Cash-out refinances are also available for VA and FHA loans. You’ve put so much love and labor into your home, and a cash-out refi lets you reap those rewards!

Streamline or Interest Rate Reduction Refinance (IRRRL): A streamline refinance could be a good option for you if you have a FHA, USDA, or VA loan. Streamlined refinances and IRRRLs reduce how many items (such as an appraisal or credit check) are needed for eligibility, shortening the process.

Renovation Loans: The Fannie Mae Homestyle Renovation Loan, FHA 203(k), and VA Renovation are specifically for people who want to make home repairs or upgrades. One benefit of these options is that the renovation costs are rolled into the new loan amount, so there’s only one closing and one interest rate. Instead of using your home’s current value for the loan amount, your lender will use the detailed project proposal submitted by your contractor to determine your home’s “as-completed” appraised value.

Additionally, some lenders offer incentives that allow you to refinance with little-to-no fees when rates drop, making refinancing even more attractive.

When can I refinance my home?

Depending on the refinance program you choose, there may be a minimum requirement for the number of payments made or length of homeownership, though this is more often the case for loans backed by the federal government. Some conventional loans don’t have a wait time, but cash-out refis usually have a six-month waiting period. Wait times vary depending on your lender, your current mortgage, and your refinance plan. Your current equity is also a major determining factor. For example, 20% in home equity is required for most cash-out transactions. There’s also no limit to how many times you can refinance the same property if you meet eligibility requirements.

Are there closing costs?

Even though you already own your home, you may be surprised to know there can be closing costs when refinancing. Closing costs can be 2-5% of the loan amount, though this can vary. Much like the closing costs associated with buying a home, the fees for a refinance may include an origination fee, recording fee, appraisal fee, and more. Note that some refinances require an additional fee in addition to closing costs: the FHA Streamline refinances come with a mortgage insurance premium (MIP) and an upfront mortgage insurance premium (UFMIP); VA Streamline refinances mandate a funding fee of 0.5% for most cases.

How long does it take to refinance?

On average, it takes 30 days to refinance a home. The process is similar to buying a home in it involves submitting an application, providing any needed documents, going through a home appraisal in (some instances), getting underwriting approval, and attending closing. Sending correct information to your lending team on time will go a long way in speeding up the process.

No matter your reason for refinancing, it’s important to understand your goals and what’s involved with the process. Working with an experienced lending team will ensure your refi goes smoothly.

For informational purposes only. Refinancing an existing loan may result in the total finance charges being higher over the life of the loan. Veterans Affairs loans require a funding fee, which is based on various loan characteristics. LTVs can be as high as 96.5% for FHA loans. FHA minimum FICO score required. Fixed-rate loans only. W2 transcript option not permitted. Minimum required credit score of 620 for conventional loans.

Are you waiting for rates to drop so you can refinance your home? You’re not the only one! Refinancing allows you to replace your existing mortgage with another one with a different rate or conditions, and there are different types of refinances to choose from depending on your financial goals.

Rate and Term Refinance

When you think about refinancing, you likely have the rate and term kind in mind. Rate and term refinances are very popular, especially when mortgage rates drop. It can be a smart choice if you want to do any of the following: reduce your interest rate, lower your monthly payment, change the loan type (like adjustable-rate to fixed-rate), or get rid of private mortgage insurance (PMI). Note that if you want to lower your monthly payment, your loan term will be extended, while opting to refinance to a shorter term will often result in a higher monthly payment. Though each lender has different requirements, it’s best to have at least 20% in home equity with a debt-to-income (DTI) ratio of no more than 50%. The interest rates for rate and term refinances tend to be lower than that of other refinances since it’s less risky.

Cash-Out Refinance

Building equity is one of the many benefits of homeownership, but you don’t have to wait until you sell to benefit from the equity you’ve gained! A cash-out refinance allows you to transform your home equity into funds that you can use for pretty much anything. Your first mortgage is replaced with one that’s more than the remaining balance, and you receive the difference in cash. The money isn’t taxable and can be used for a number of purposes, including financing home repairs, a vacation, college tuition, or debt consolidation.

Most lenders will let you borrow up to 80-85% of your home’s appraised value, as long as you retain at least 20% equity. Since your new mortgage will be more than your initial one, expect the interest rate and your monthly payment to be higher. The rates for cash-out refis tend to be slightly higher than for rate and term refinances since they carry more risk. Cash-out refinances are available for conventional mortgages, VA, and FHA loans, with varying seasoning or waiting periods. For conventional loans, you’ll need to have owned your home for at least 6 months and have your current mortgage be seasoned for 12 months. VA loans have a 210-day seasoning period, and FHA loans have a 12-month requirement for primary ownership and occupancy before applying for a cash-out. FHA refinances also have mortgage insurance premiums (MIP). If home values in your area have risen greatly, a cash-out refinance can be an excellent way to get in on the appreciation boom!

Do you still love your home but feel it could use some upgrades? The FannieMae Homestyle Renovation Loan, FHA 203(k), and the Freddie Mac Choice Renovation loans all blend the perks of a rate and term refinance with the capital needed to repair or update your home. Renovation loans are especially convenient because the refinance of your current loan and repair costs are combined into one loan; it only has one closing and interest rate, and it provides flexibility when it comes to what can be updated. Unlike a home equity line of credit (HELOC), second mortgage, or cash-out refinance, which all use the home’s current value to determine the amount that can be borrowed, the renovation loan is based on the home’s after improved value. To determine the after-improved value, your contractor must submit a detailed plan of what’s to be fixed and how much it will cost. The appraisal is then completed using the contractor’s bid to determine what your home will be worth after the renovations are completed. Renovation loans are ideal for projects like building an addition, improving kitchens and bathrooms, and updating your home’s utility systems.

Streamline Refinance

Who says refinancing has to be a hassle? If you have an existing FHA, VA, or USDA loan, you may have the option of going with a streamline refinance. Streamline refinances are just what their name implies—they’re a simplified refinance that speeds up the process. With this kind of refi, it’s common for income documentation, home appraisal, credit requirements to be absent or very relaxed. Each of the three varieties of streamlined refinances has unique traits:

FHA

The FHA streamline refinance doesn’t require a credit check, appraisal, or income verification and has flexible loan-to-value (LTV) and debt-to-income (DTI) requirements, making it an attractive option. If 210 days have passed since closing on your first mortgage and you’ve made at least six mortgage payments, you’ll be ready to look into an FHA streamline refi. Like the normal FHA loan, the streamline refi involves paying a MIP for the life of the loan and a one-time upfront mortgage insurance premium (UFMIP).

VA

Also called an interest rate reduction refinance loan (IRRRL), the VA streamline refinance has no appraisal requirements or employment verification. Be sure to budget for the 0.5% funding fee and closing costs. You can apply for an IRRRL if you’ve made 6 monthly payments to your first mortgage and 210 days have passed since the initial closing. The borrowing limits are very generous and allow you to refinance up to 120% of your loan’s value. The IRRRL is only available to use for a rate-and term refinance, cash-outs are not allowed.

USDA

A USDA streamline refinance loan lets you refinance without going through a credit check, DTI verification, home inspection, or appraisal. To be eligible, you’ll need to have made at least 12 on-time payments towards your first loan. Like the IRRRL, the USDA streamline can only be used to obtain a rate and term refinance.

People refinance for a number of reasons, so it makes sense to have a variety of refinance options available to help you achieve your financial goals. Working with an experienced loan originator and choosing the right refinance for your needs will help ensure you’re getting value out of your home purchase for years to come.

For informational purposes only. Refinancing an existing loan may result in the total finance charges being higher over the life of the loan. Veterans Affairs loans require a funding fee, which is based on various loan characteristics. LTVs can be as high as 96.5% for FHA loans. FHA minimum FICO score required. Fixed rate loans only. W2 transcript option not permitted. Minimum required credit score of 620 for conventional loans.

When interest rates are low, it seems like everyone is refinancing their home. If you’re already a homeowner, refinancing can be a great way to lower your monthly payment, make home repairs, or pay off your mortgage faster. Here are 7 things to know about refinancing.

What is Refinancing?

When you refinance your home, you’re replacing your original mortgage with a new one. Oftentimes, the new mortgage will have a lower rate or term than your previous one, and in some cases that’s required. In some ways, refinancing can be easier than buying a property since you’ve already bought your home, but has its own unique considerations.

1. Improve Your Credit Score* and DTI

Just like when you were buying your home, your credit score will be a significant factor when you decide to refinance. It’s best to have a have a credit score within a healthy range, though credit requirements will vary depending on your lender and the loan program you choose. Take steps to improve your credit score so you can be in the best position when you refinance. Your lender will also look at your debt-to-income ratio, or DTI. The lower your DTI, the more reliable you’ll appear to lenders since your debts don’t exceed your pre-tax income. A DTI at or under 36% is generally favorable, but the requirement will differ between lenders. Paying down large debts can help you reduce your DTI in preparation for a refinance.

2. Know Your Reason to Refinance

Refinancing is attractive for people who are already homeowners, but not everyone refinances for the same reason. Some common refinance goals include changing the loan’s rate and term or getting rid of PMI. The refinance process will vary depending on what your objective is, so knowing what you want out of your refinance will help you prepare accordingly.

3. Gather Documentation

Collecting all the needed documentation for a refinance can be tedious and time consuming, so having an understanding on what to provide can make your refinance smoother. To verify income and employment, bring the last 2 months of pay stubs and 2 years of tax returns/W-2s to show your lender. Note that Social Security payments, pensions, disability, alimony, and child support are considered sources of income. You’ll also need to bring statements outlining all your assets and debts. Don’t forget to show proof of home insurance, as most lenders require that you have it when refinancing. Be sure to stay in close contact with lender in case there are other documents you need to provide or explain.

4. Know Your Break-Even Point

One of the most common questions homeowners have about refinancing is. “Is it worth it?” Although each situation is different, calculating your break-even point can help answer this question. The break-even point is when you begin to save money after the refinance. You can calculate the break-even point using a calculator, or by dividing the total cost of your refinance by your monthly savings to get the number of months needed to recoup your money. You should also consider how long you plan to stay in your home. For example, if you’re thinking of moving in the near future, refinancing might not make much sense. After you have an estimate of your break-even point, consult with your lender. Nothing beats meeting with a Loan Originator (virtually or in-person) to discuss the best refinance plan for you.

5. Don’t Forget Closing Costs

Even though refinancing can save you money in the long run, there are still some immediate expenses to consider during the process. Closing costs aren’t just for buying a home, they’re part of refinancing, too. Closing costs can include an appraisal fee (if you have one), origination fee, title fee, and the lender’s attorney. You can expect 2-5% of your refinancing costs to go towards closing, so be sure you have enough money to account for them. Your lender may allow you to have a no-costs closing where the closing costs are rolled into your refinance. In a no-costs closing, your closing fees are either added to the principal or exchanged for a higher interest rate.

6. Lock in Your Rate

Locking in an interest rate is a smart move, especially when you’re refinancing. If you come across a low rate, locking it will prevent it from fluctuating, potentially saving you a lot of money as you pay off your refinance. If you want to lock your rate but are concerned about missing out on an even lower rate, ask your lender if a float-down option is available. When current rates are low, you don’t want to miss the opportunity to protect it.

7. Prepare for a Home Appraisal

A home appraisal helps your lender know your home’s current value and informs them how much they are reasonably able to loan you. An appraiser from a third party will visit your home and make note of its condition, along with comparative data from your local area. Then, they send a report to your lender who will consider the information when processing your application.

COVID-19 has caused many home appraisals to be done with software instead of physical visits, but you should still be prepared to have your home appraised. If you’re having a virtual appraisal, treat it like you would an in-person appointment. Take time to do some cleaning, repair and replace fixtures as needed, and tidy up your yard to give it curb appeal. Some lenders may be willing to offer an appraisal waiver; it doesn’t hurt to ask if it’s an option.

Much like applying for a mortgage, there is no one-size-fits-all way to refinance. Knowing your reason for refinancing and getting in shape financially will help you have a successful and smooth refinance experience.

*NFM Lending is not a credit repair company. Please contact a credit repair company for more information on how to improve your credit score.Refinancing an existing loan may result in the total finance charges being higher over the life of the loan.