It’s normal to feel confused and a bit overwhelmed when buying your first home—it’s a complex process with many moving pieces. To make your inaugural homebuying experience smooth and successful, here are some common mistakes to avoid when buying your first home.

Not Getting Pre-Approved First

If you’re seriously in the market to buy a home, getting pre-approved with a lender first is a must! A pre-approval involves submitting various financial documents and proof of identity to your lender, as well as allowing them to run a hard credit check on you. A pre-approval differs from pre-qualification in that the former takes a more comprehensive look into your finances and is a hard credit inquiry (your score will drop slightly temporarily); a pre-qualification just gives you a rough estimate on whether you can afford a home based on self-reported information. A pre-approval also has much more weight when you’re house hunting and gives you an idea of how much home you can afford. If you’ve found a home you love, having a pre-approval letter makes you seem like a more serious buyer and can help move the mortgage process along more quickly. Be aware that pre-approval letters are good for 60-90 days, and you’ll need to go through your lender to get an updated one after the first one expires. Once you’re pre-approved, you can find a great real estate agent and shop with confidence!

Buying More House Than You Can Afford

Being able to buy a house is one thing, being able to keep it is another. When your lender comes back with the pre-approval, you’ll be given a figure for the maximum amount you can borrow. Depending on whether you use less than the max or the full amount, that will be reflected in your monthly payment. However, even if you’re approved for a larger sum of money, it’s not always a good idea to go to the limit. A good rule of thumb is to not spend more than 28% of your gross income on mortgage payments. When a significant amount of your paycheck goes to your mortgage, you become house poor. The amount you’re comfortable borrowing is a personal decision, so make sure you have the cash flow to support regular mortgage payments, as well as other homeownership costs.

Overlooking Other Costs

Becoming a homeowner is a huge life change, both personally and financially. If you’ve only ever rented, you might be surprised at just how much owning a home costs. Aside from your regular mortgage payments, you’ll need to account for escrow payments (property taxes and home insurance), regular maintenance costs, and emergency repairs, and sometimes private mortgage insurance (PMI). If your home is part of a homeowner’s association (HOA), expect to pay yearly or monthly dues. Seeing as most of these costs are variable and unpredictable, it’s wise to create separate savings just for home expenses. Try putting aside money as you prepare to begin the homebuying process or after you’ve closed on your home.

Jeopardizing Your Closing

When your lender tells you closing is around the corner, you’re basically home free, right? Not exactly. Your mortgage and home purchase haven’t officially been finalized, so it’s crucial to maintain your credit score, cash supply, and debt-to-income (DTI) ratio until then. Activities to avoid before closing include: quitting your job, applying for or cosigning a loan, applying for a credit card, closing lines of credit, and making large, unnecessary purchases (like buying or leasing vehicles, furniture, or expensive trips). Doing these things can delay or even make you ineligible for mortgage approval. If you’re in what you feel is an emergency situation, contact your loan originator right away and tell them what’s happening. They’ll let you know how best to proceed in a way that won’t threaten your closing.

Using the Wrong Real Estate Agent

Choosing the right real estate agent for your needs is important any time you’re buying or selling a home, but especially if you’re a first-time buyer! Don’t pick just any real estate agent to help you buy your first time—be sure to thoroughly interview and research several local agents. When interviewing agents, ask about their communication style, familiarity with the area, industry experience, local market trends, and reviews from past buyers. Additionally, if you’re using a specialized mortgage to purchase your home (such as a VA loan), seek out agents who are well versed in working with buyers like you. Besides their technical know-how, the strong agent should also be a good listener and friendly.

Buying a home comes with many challenges, and even more so if you’ve never done it before. Fortunately, there are many factors you can control that will mean the difference between having an exceptional home buying experience instead of an exasperating one.

About NFM Lending

NFM Lending is a national mortgage lending company currently licensed in 49 states in the U.S. and Washington, D.C. The company was founded in Baltimore, Maryland in 1998. NFM Lending and its family of companies includes Main Street Home Loans, BluPrint Home Loans, Elevate Home Loans, and Element Home Loans. They attribute their success in the mortgage industry to their steadfast commitment to customers and the community. For more information about NFM Lending, visit www.nfmlending.com, like our Facebook page, or follow us on Instagram.

For many aspiring homeowners, coming up with a down payment is a significant obstacle standing in the way of homeownership. While having a 20% down payment isn’t required to buy a home, it can be challenging to gather enough funds to start the home buying process. Read on to learn about different ways to come up with a down payment.

Increase Savings

Saving money is perhaps the obvious first choice when it comes to collecting a down payment. The process of putting away extra money usually happens gradually, so it’s best to start a dedicated savings account as soon as possible. Increase your savings potential by creating and maintaining a household budget. You might also consider starting a side hustle or asking your employer for a raise to increase your cash flow. Growing your savings will be beneficial when you’re ready to begin your home buying journey, even if you find you won’t need much for your down payment.

Down Payment Assistance

Down payment assistance (DPA) programs are an underrated way to partially or fully subsidize your down payment. There are many DPA programs offered to homebuyers at the federal and state level, from both public and private institutions. DPA programs are often tailored to first-time or low-income buyers, but repeat homebuyers may be eligible for certain programs. The DPA funds can come in the form of a grant or a low interest second mortgage that may be repayable or forgiven after a set amount of time. If you’re part of a particular profession, such as teaching or law enforcement, there are DPA programs designed to help you become a homeowner. Taking advantage of DPA allows you to secure your dream home and save for other expenses. Make sure to ask your loan originator if you qualify for any down payment assistance programs.

Gift Funds

Your down payment doesn’t have to come entirely from you; all or part of it can come from family and friends in the form of gift funds. In order to use gift funds in your down payment, have your benefactor send your lender a gift letter detailing the amount given, their relationship to you, withdrawal dates, and a statement that repayment is not expected. Your lender may also need to see accompanying withdrawal and deposit slips to source the money. It’s important to know that if your contributor expects you to repay the gifted money, it will be considered a loan and will be factored into your debt-to-income (DTI) ratio.

Leverage Your 401(k)

401(k)s are meant to be accessed upon reaching age 59 ½ , but tapping into it earlier can boost your down payment amount if needed. You can either use a 401(k) loan (if offered by your employer), or withdraw funds. Both methods allow you to access cash on hand without going through a lender or credit check. A 401(k) loan lets you borrow against your retirement savings and must be restored within five years with interest. Your employer may pause 401(k) contributions until the loan is paid back. Withdrawing money from your account will lead to a 10% penalty fee, and any amount you remove will be subject to an income tax. You will also forfeit any tax-free retirement earnings that you have accrued. For these reasons, this option is best used only as a last resort. It’s essential to consult with a financial advisor so you fully understand what’s involved.

Getting a down payment ready doesn’t have to be the thing that stops you from achieving homeownership! If owning a home is something you want to accomplish, it’s ever too early to start saving and preparing for one of the most important purchases of your life.

If you have any questions about buying a home, contact one of our licensed Mortgage Loan Originators. If you are ready to begin the home buying process, click here to get started!

NFM Lending is not a financial or tax advisor. You should consult a financial advisor to assist with your financial goals.

Note: This blog was originally published in June 2013 and has been updated.

Reaching the closing stage in the homebuying process is always exciting! Closing officially marks the beginning of your new life in your new home, but there’s more involved than just getting the keys–here’s what you can expect at closing.

Final Walkthrough

A few days before attending closing, you need to perform a final walkthrough of the home with your real estate agent. Final walkthroughs give you the opportunity to ensure there are no outstanding issues with the property and that the sellers made appropriate repairs if they were part of the negotiation. Check that major appliances, electricity, HVAC systems, and plumbing work properly. If you find something that needs to be addressed, it may delay the sale. Regardless of the home type or whether it’s a new build or is pre-owned, doing a final walkthrough is highly encouraged. It’s better to check beforehand than to sign the papers and discover a problem when you move in.

Reviewing and Signing Documents

At least three business days before your closing date, you’ll receive a closing disclosure (CD) from your lender. The CD gives a breakdown of your loan terms, loan costs, closing costs, projected payments, cash needed at closing, and more. Review your CD carefully to ensure you understand the loan terms and that everything is accurate. Even something as seemingly insignificant as a misspelling will be an issue if left uncorrected. If you see any errors or have questions, contact your loan originator immediately.

When you arrive at the closing table, bring a valid photo ID and proof of homeowner’s insurance. These will be needed to verify your identity and show that the property is protected from accidents. On closing day, you’ll be signing more key documents in the loan package, like the promissory note, the mortgage itself, the deed, title transfer papers, the bill of sale, and the notice of servicing disclosure. Your lender and real estate agent should inform you of all the documents you’ll need to sign and what they mean prior to closing. Let your real estate and lending team know if you see errors or are unsure about anything.

Pay Cash to Close

The cash to close consists of closing costs, the down payment, and prepaid costs (like HOA dues), minus any credits you receive. You’ll know the exact figure from the details in your CD; contact your lender if you see a mistake. If you’re paying any of these costs out-of-pocket, bring a cashier’s or certified check, or have the amount wired to the title company a day or two before closing. When doing a wire transfer, avoid scams by confirming the address directly with your title agent. After the money has been disbursed and all the documents have been signed,the property transfer will be complete. The title company or real estate attorney will submit the documents to your local government’s public land records for recording. Congratulations—you just closed on your new home!

It takes a lot of hard work to get to the closing table, so celebration is definitely in order! No matter how eager you are to finish signing papers and get your keys, it’s imperative to take your time reading everything thoroughly. Having everything in order before the closing date will help reduce last-minute snags or surprises.

If you have any questions about closing, contact one of our licensed Mortgage Loan Originators. If you are ready to begin the home buying process, click here to get started!

If you have questions about closing on a home, contact one of our licensed Mortgage Loan Originators. If you’re ready to begin the home buying process, click here to get started!

Declaring bankruptcy is financially and emotionally stressful—it’s a situation no one wants to be in. Filing for bankruptcy is a tough decision, but you can bounce back from it and even become a homeowner.

Bankruptcy Types

Individuals can either file for Chapter 7 or Chapter 13 bankruptcy, and they have different implications for your finances and when you can start the mortgage process. After the initial filing, a bankruptcy court can declare it as discharged (eligible debts are removed) or dismissed (the court is not proceeding with bankruptcy filings because of unmet requirements). Your bankruptcy status plays a large role in your timeline for mortgage application.

Chapter 7 Bankruptcy

When you file for Chapter 7 bankruptcy, certain assets are sold to repay creditors, and any leftover debt is discharged. This is the more severe of the two, and the bankruptcy will remain on your credit report for 7 years. You’ll need to wait a minimum of two years before applying for a mortgage, but it can be more depending on the loan program. The wait is two years for FHA and VA loans, three years for USDA loans, and four years for conventional loans. Individual lenders may set their own waiting periods, as well. The waiting period starts after your bankruptcy is dismissed or discharged.

Chapter 13 Bankruptcy

Chapter 13 bankruptcy is not as extreme as Chapter 7; you can keep your assets and must adhere to a court-ordered debt repayment plan. As long as you continue making payments, your assets won’t be seized. It stays on your credit report for 7 years, but the waiting period to get a mortgage can be as little as 1-2 years depending on the loan program, the status of your bankruptcy (dismissed or discharged), and lender requirements. For FHA, VA, and USDA loans, you have to be at least one year into your repayment plan before trying to get a mortgage. For conventional loans, you must wait two years after your bankruptcy was discharged, and 4 years after a dismissal. Generally, you’ll need the court’s approval before applying for a mortgage if you’re still in Chapter 13 bankruptcy.

Improving your Finances

No matter what type of bankruptcy is on your record, it’s crucial to take measures to rebuild your finances and make smart financial choices. The mandatory waiting period is a prime time to improve your credit profile and show lenders that you’re responsible and financially secure enough to handle a mortgage. First, create and stick to a budget that covers your basic needs and any recurring bills. Gradually, you should ideally see more money in your pocket. Put some of that extra cash into savings so it can be used for a down payment or other housing costs. Strengthen your credit score by always making on-time payments, paying in full whenever possible. Don’t max out your credit cards or apply for new ones to keep spending. Avoid taking on unnecessary debt, and lower your debt-to-income ratio (DTI) by paying down existing debts. Repairing your finances won’t happen overnight—it takes time and consistent work.

Things to Consider

When you’re in a better position to start the homebuying process, government-sponsored loans are an excellent choice to consider, as the waiting periods are shorter and have more flexible requirements than conventional loans. Bankruptcy can be caused by a number of issues, both within and outside of your control. Some loan programs may reduce the waiting period if your bankruptcy was caused by a one-time, extenuating circumstance that is well-documented (such as a medical emergency). You might need to provide your lender with a letter of explanation if an extenuating event caused your bankruptcy. Regardless of what type of bankruptcy is on your record, speak with a loan originator to see what options are available for your situation.

Bankruptcy may feel like a death sentence, but it doesn’t have to be. The speed bump that bankruptcy puts in front of homeownership can be used to your advantage by taking steps to restore your finances. When you’re financially, mentally, and emotionally prepared for homeownership, you’ll be set up for success.

If you have any questions about the home buying process, contact one of our licensed Mortgage Loan Originators. If you are ready to buy a home, click here to get started!

NFM Lending is not a debt settlement company or credit repair agency. Speak with a licensed financial advisor regarding your unique financial situation.

LTV’s can be as high as 96.5% for FHA loans. FHA minimum FICO score required. Fixed rate loans only. W2 transcript option not permitted. Veterans Affairs loans require a funding fee, which is based on various loan characteristics. For USDA loans, 100% financing, no down payment is required. The loan amount may not exceed 100% of the appraised value, plus the guarantee fee may be included. Loan is limited to the appraised value without the pool, if applicable. Qualifying credit score needed for conventional loans.

Every homebuyer wants a great mortgage rate, but what exactly goes into how the rates are set? No, it’s not astrological movements or cloud formations; it’s a variety of financial and economic elements. Learn how these factors impact how mortgage rates are determined.

Your Finances

Credit Score

You don’t need a “perfect” credit score to buy a home, but having a strong score gives you access to more competitive interest rates and programs. Your credit score is a significant metric in predicting how likely you’ll be able to pay back the mortgage. Even if you’re not thinking of buying a home in the near future, build up your credit score now so it’s primed for when you’re ready.

Debt-to-Income Ratio (DTI)

Having a high debt-to-income ratio (DTI) means you have little money left after paying your current bills, and it can lead to paying higher interest rates. Take steps to pay off debts, especially high interest ones like credit cards.

Loan-to-Value Ratio (LTV)

The loan-to-value ratio (LTV) also factors into your rate. If you’re seeking a mortgage that covers over 80% of the home’s price, it’s considered a high LTV and is considered riskier. You’re more likely to be offered a lower rate if your LTV is 80% or under, and you won’t need to pay private mortgage insurance (PMI).

Down Payment

Though having a 20% down payment is not necessary for all home buying programs, the amount you’re able to contribute to a down payment can affect your mortgage interest rate. Lenders view borrowers who can put down more money upfront to be less risky, and can offer lower rates. The down payment amount can also lower your LTV.

Mortgage Points

Though it is entirely optional, paying mortgage points at closing (aka, buying down the rate) is another way to lower your interest rate. One point equals 1% of your mortgage, and buying additional points will minimize your rate even further. The discounted rate stays with the loan until you refinance or pay it off.

Federal Reserve Actions

The Federal Reserve is always a hot topic whenever mortgage rates shift, but they don’t actually set mortgage rates. Instead, they determine the federal funds rate, which is how much interest banks are charged for borrowing from the Fed and when exchanging money with other depository institutions. The Fed considers various market indicators when they decide to change the federal funds rate. These factors include: economic growth, inflation, unemployment, the housing market, and the overall health of the economy.

The funds rate has a direct effect on rates for adjustable-rate mortgages (ARMs), home equity lines of credit (HELOCs), and home equity loans, all of which are based on an index. When it comes to fixed-rate mortgages, the funds rate has a more indirect impact as it can spur demand in the bond market. For example, a lower funds rate boosts bond prices and investor demand, leading to lower mortgage rates. Conversely, increasing the funds rate can lessen bond prices and demand, resulting in higher mortgage rates.

The Bond Market

Mortgages are largely based in the mortgage-backed securities market (investors buy groups of mortgages), which is influenced by U.S. Treasury securities (government bonds). Bond prices and rates have an inverse relationship, and shifts in the bond rate often cause similar movements for fixed-mortgage rates. Mortgage lenders use bond market activity as a guideline to set their lending rates.

Your Lender and Loan Programs

Another thing that makes mortgage rates hard to pin down is that lenders have different criteria for eligibility and don’t all offer the same programs and incentives. Rates and requirements are not uniform across all loan programs. Mortgages with shorter repayment terms tend to have lower rates than those with longer terms, but the monthly payment is usually higher. When deciding which lender and mortgage program to work with, be aware that the advertised rate may reflect a best-case-scenario and can differ from what you may be eligible for. Be sure to work with a loan originator to see what options are available for your unique situation.

There’s no such thing as a universal mortgage rate; rates differ depending on individual circumstances, economic conditions, lenders, and loan programs. Even though you can’t control every aspect that affects interest rates, it’s important to manage the ones you can. Working with a reliable lender and improving your finances will give you an edge when you’re ready to buy a home.

If you have any questions about using mortgage points, contact one of our licensed Mortgage Loan Originators. If you are ready to begin the home buying process, click here to get started!

Paying property taxes each year is part of the reality of being a homeowner, but there’s a way you could minimize this expense. A homestead exemption can save you money on your property taxes, and you don’t need to be a farmer to take advantage of it! Learn what the homestead exemption is and how it can give you a break on your taxes.

What is the Homestead Tax Exemption?

The homestead exemption benefits homeowners by offering two things: protection from certain creditors in case of bankruptcy or the death of a spouse, and a reduced property tax. We’ll be discussing the latter here. Property tax is determined by your home’s assessed value, which your local government determines based on several factors. The homestead exemption reduces how much of your assessed value gets taxed, potentially saving you hundreds of dollars in taxes.

For example, if your home’s assessed value is $250,000 and your property tax totals 1%, you would pay $2,500 in property taxes. However, if you have a homestead exemption of $20,000, only $230,000 of your home would be taxed, lowering your property tax to $2,300 and saving you $200.

The deduction amount varies widely by state and county; sometimes it’s a flat amount or a percentage of your assessed value or acreage. Having a homestead exemption in effect is beneficial outside of the upcoming tax season—it gives you a cushion against rising property values since you won’t have to pay the full amount.

Eligibility

Each participating state and county will have their own specifications, but a general requirement for eligibility is that you own your home and live in it as your primary residence. You can’t receive an exemption on a second home or investment property, and you’re limited to one per household. If you’re also part of a special population, such as being a senior citizen, a Veteran or surviving spouse, or disabled, you may qualify for additional property tax exemptions. Applying for the homestead exemption usually involves sending proof that you live in and own your home. Some local jurisdictions may require you to refile for an exemption each year, but some may not. If you move, you’ll have to file a new application. Similarly, if you bought a home within the past year, apply for a homestead exemption as soon as possible to reap the tax benefits. Be sure to consult a tax advisor for your area’s terms and eligibility requirements.

Few people like paying property taxes, but having a homestead exemption can ease your tax burden. It’s simple to find out whether you qualify, and any tax savings will truly add up when all is said and done.

If you have any questions about the home buying process, contact one of our licensed Mortgage Loan Originators. If you are ready to buy a home, click here to get started!

Terms and requirements vary by location, programs may not be available in all areas. NFM Lending is not a tax advisor. You should refer to a licensed tax advisor and your local area’s department of assessment and taxation regarding your unique financial situation.

In many ways, the home buying and selling process isn’t too different from dating. There’s back-and-forth discussions, compromises, trial and error, and the all-important profile pics (listing photos). In today’s digital world, using online multi-listing sites (MLS) is the most common way buyers shop for homes. Use these simple staging tips to get buyers to “swipe right” on your home.

Clean Up

A clean home is a basic, yet crucial part of prepping your home to sell. When your home is clean and organized, it conveys to buyers that you take care of your property and that the home is pleasant to live in. Start decluttering your belongings to make organizing easier. If you have something that you hardly use or has lived past its usefulness, donate, sell, or toss it. Then, give your home a deep clean. Carpeted areas may benefit from professional cleaning if they still look dingy after vacuuming. In addition to the areas you usually clean, pay attention to baseboards, walls, shelving, and ceiling fans. These areas may not get cleaned often, but the dirt and dust can be apparent in photos. Next, polish up your home by organizing it. Make sure all the beds are made (no laundry piles allowed!) and that closet doors are closed. Clear the countertops in your kitchen and bathrooms from excessive appliances and personal care products. You want to show off all the counter space in your home, not hide it under a bunch of clutter! Store away piles of papers or organize them properly in a file sorter. Look at your bookcases—are the books stacked upright or laying wherever? Stand books up correctly and neatly. Never leave piles of clothes or knickknacks on the floor, as this looks sloppy and reduces visual floor space.

Decorate Strategically

Showcasing your personality is a key goal when creating a dating profile, but not so much when you’re staging your home. Buyers want to picture themselves living in your home, and it can be difficult to do that when you have family photos plastered everywhere. Go around your home and remove personal items from being displayed, including personal photos, your child’s drawings from the fridge or walls, and religious and political decor. Depersonalizing doesn’t mean your house needs to look boring and sterile—a few well-placed decor pieces can enhance your staging. Try using some cute, affordable throw pillows to jazz up seating. Natural elements are always a good staging accessory, and you can incorporate subtle seasonal elements into your home. A few real or faux houseplants on floors or tables adds a touch of greenery to your home, and it looks attractive no matter the season. Place vases of real or artificial flowers or bowls of fruit on tables to give a look of freshness. If you’re trying to make a room seem larger, hang a large mirror to give the illusion of increased space. Make sure your TV is turned off during staging photo sessions so as not to be a distraction.

Shed Some Light

Everyone knows the key to a great profile picture is good lighting, and the same goes for staging. Luckily, you don’t need fancy lighting equipment! Open your blinds to let the sun in, and leave the lights on for photos. If your existing lights aren’t brightening the room enough, consider replacing the bulb, as older bulbs dim over time. Pay attention to the warmth or coolness of the bulb, too. Warm light is yellow-tinged and less intense, while cool light is blue-toned and more intense.

Curb Appeal

Does your house look welcoming from the outside? A home that appears well-kept from the street draws buyers in and is one of the first pictures buyers see when browsing MLS sites. Your front porch is a prime area to add curb appeal. Try repainting your door, placing potted flowers near the stoop, and hanging a wreath on the door. It’s a good idea to clean the grime from your siding; check if the material is safe for power washing. Cleaning windows from the inside and outside will give your home extra sparkle; don’t forget the screens! For the surrounding land, trim overgrown grass, bushes, and tree branches. If you have fencing along your property, ensure there are no missing or damaged slats, and repaint panels if needed.

Don’t let poor or nonexistent staging hurt your home’s sale potential—show that your house is “forever home” material! Effective staging should make your home look like someone could live there, but doesn’t look lived in. You don’t have to spend a fortune—cleanliness and a little creativity can go a long way when selling your home.

If you want to know more about how to pay off your mortgage faster, contact one of our licensed Mortgage Loan Originators. If you are ready to begin the home buying process, click here to get started!

Credit: Featured image created with Image by rawpixel.com on Freepik

Flooring is anything but boring! The type of flooring you choose for your home contributes to your home’s aesthetic and comfort—it shouldn’t be an afterthought! If you’re debating what flooring you should use in your home, read up on these different types of flooring.

Carpet

Not a fan of having to walk on cold, hard floors? Carpeted floors are what you want! Carpets come in a rainbow of colors to coordinate with your decor, as well as various textures and densities. Common carpet types include loop pile, plush pile, frieze, Berber, and twist pile. Aside from aesthetics, the carpet’s characteristics impact its durability and care. Padding is placed under carpet during installation; choose carefully, as the padding affects the carpet’s longevity and your walking comfort. Many brands offer stain resistant carpeting, but clean up messes as soon as possible to prevent permanent stains or smells. Regular vacuuming is sufficient for regular cleaning, but have your carpets deep cleaned once a year to remove embedded dirt. Carpeting often ranges from .65 cents-$12 per square inch, making it a very affordable choice.

Standard and Engineered Hardwood

Hardwood has an irreplaceable warmth and feel—it’s a true classic! Being made of solid wood, hardwood handles foot traffic well and can be refinished multiple times. With proper care, it can last generations. Be sure to dry dust regularly, use wood floor-friendly cleaning products, and dry well afterwards. Moisture doesn’t play well with hardwood, so avoid installing it in bathrooms and kitchens, and wipe up spills quickly. Hardwood tends to cost around $6-18 per square foot with installation, though engineered hardwood can be a good alternative.

Engineered hardwood is composed of several thin layers of wood, topped with a veneer of real hardwood. This gives you the hard-to-replicate look and feel of hardwood. If the veneer is thick enough, it can be refinished 1-2 times during its lifetime. This flooring type typically ranges from $3-11 per square foot but can be more depending on the quality. Sweep floors clean or use products designed for engineered floors. Like hardwood and laminate, don’t let water sit on the surface for long or install in humid areas.

Vinyl

For homeowners looking for durable, low-maintenance flooring that’s easy to maintain, vinyl is an excellent choice. Vinyl can be made to look like other materials, and it works well in high traffic areas or in high moisture areas. The most common forms of vinyl flooring are sheet, tile, and plank. Vinyl sheets and tiles need to be glued to the floor’s underlayment, but planks can snap together to be laid over the existing floor. Vinyl floors are either waterproof or water resistant, making cleaning a breeze. The price per square foot ranges from .50 cents to $10, depending on the type and quality. Keep in mind that vinyl isn’t the most eco-friendly option since it’s synthetic, and removing glued-on flooring is difficult.

Stone and Ceramic Tile

Stone and ceramic tile floors add a touch of sophistication to your home and can last for decades with the right care. Popular types of stone flooring include marble, granite, limestone, and slate. It’s compatible with every room in your home and handles foot traffic well. Because stone is porous, the surface needs to be sealed to prevent water damage. Depending on the material and location, resealing should be done every 18 months or 3-4 years. Bathroom and kitchen floors may need to be resealed more often due humidity levels. To preserve the stone’s unique characteristics and finish, use mild, non-abrasive cleaning products and clean up messes quickly. Stone is among the pricier flooring types; expect to pay $8-40 per square foot.

Ceramic and porcelain floors are available in many shapes, colors, and patterns to give your home flair. Both materials work well in damp areas, are hygienic, and quite durable against scratches. Though they’re sturdy, they aren’t immune to damage. Tiles can crack if something extremely heavy falls on them and may chip at corners. Basic cleaning can be done with a mild solution, though it’s a good idea to scrub any grout lines every so often to prevent dinginess. While the tiles themselves don’t require sealing (most come glazed), cement-based grout should be sealed to protect the integrity of your flooring. Ceramic tiles start around $1-6 per square foot, and porcelain is about $3-9. Be aware that flooring and installation costs will be higher if you’re using nonstandard tile shapes or want an intricate layout.

Laminate

Laminate floors are a cheaper alternative to hardwood floors and feature a printed veneer over a wood composite base. At around $3-8 per square foot, it’s a great option if you want the look of hardwood on a budget. You can even install it yourself! Laminate flooring has come a long way and is more durable than in the past. When shopping for laminate, pay attention to its abrasion criteria (AC) rating. The AC rating shows how durable it is in relation to how much foot traffic it will receive. Avoid installing in areas with high humidity, as the floor can warp. Caring for laminate requires care and vigilance; never clean with a wet mop or let liquids sit too long on the surface, as it can damage the floor. Instead, use a broom or a laminate-friendly cleaning solution to maintain it.

Flooring has come a long way to make our homes more attractive and complementary to our lives. When shopping for flooring, always keep your budget, lifestyle, home aesthetic, and the installation area in mind. Be sure to take home samples to compare quality. Well-chosen flooring is sure to enhance your home and make you love it even more!

If you have any questions about the home buying process, contact one of our licensed Mortgage Loan Originators. If you are ready to begin the home buying process, click here to get started!

The Veterans Affairs (VA) loan is just one benefit military members can use as a reward for their service. Its generous terms and flexible requirements have helped numerous families achieve homeownership, but there are still things many people get wrong about the VA loan. Here are some of the most common myths about the VA loan, debunked.

Myth: The VA loan is Only for Active-Duty Military and Veterans

You wouldn’t be wrong if you thought active-duty service members and veterans were the most prominent beneficiaries of the VA loan, but they aren’t the only populations that can use it. National Guard and Reserve members may be eligible for a VA loan if they have served six or more years or have at least 90 consecutive days of active duty, as well as an acceptable type of discharge as determined by the VA. Surviving spouses may also be able to use a VA loan if they can obtain a certificate of eligibility (COE) and meet certain conditions, like remaining unmarried at the time of application and if the Veteran died while serving or due to a service-related disability.

Myth: The VA Loan is Bad for Sellers

The VA loan has made homeownership possible for millions of military families since 1944, but there are still sellers who are wary of it. Some believe that because VA loans don’t require a down payment or private mortgage insurance (PMI), military buyers are riskier. This couldn’t be further from the truth. VA financing can fully cover the mortgage prices in many cases, and it will guarantee up to 25% of the loan in case of default. VA buyers also have more money to put towards the offer.

Another misconception is that sellers have to pay all of the buyer’s fees at closing. To maintain affordability, the VA limits homebuyers from paying certain unallowable fees. The VA states sellers have to pay for a termite inspection, real estate agent fees, brokerage fees, and buyer broker fees. There are more closing costs that VA buyers can’t pay, but that doesn’t mean the seller is obligated to pick up the tab for all of them. Lenders and agents may cover some of the unallowable fees, and buyers can negotiate with sellers to pay them. It’s important to note that sellers can’t pay more than 4% in seller’s concessions for a VA loan.

Myth: VA Loans Have No Closing Costs

Even with the cost-saving features of the VA loan, it’s not entirely a free ride. There are still closing costs, including a funding fee unique to the VA loan. The funding fee is a one-time payment that helps reduce taxpayer expense to fund the loan. The fee ranges from 1.4-3.6% of the loan amount depending on the down payment amount. Though a down payment isn’t required, the more you can contribute, the lower your fee. You can pay it upfront at closing, roll it into your mortgage, or ask the seller to pay it. For any subsequent uses of your VA loan, the funding fee can be higher if you have a down payment less than 5%. There are a few situations in which the fee may be waived, like in cases of a service-related disability or for an eligible surviving spouse. If you’re concerned about closing costs, consider asking your lender for a lender credit or negotiate with the sellers for a contribution. Again, sellers can pay up to 4% in closing costs.

Myth: The VA Appraisal is Too Strict

The mandatory VA appraisal is another thing that makes the VA loan distinct from other loans, and many people are intimidated by it. Properties need to have an appraisal done to assess fair market value and the home’s safety and sanitary conditions. The appraisal is not the same as a home inspection, as a true inspection is more thorough. An independent appraiser will review the home against the VA’s list of minimum property requirements (MPRs). Issues appraisers will look for include exposed wiring, termite damage, and adequate drainage. If the home doesn’t meet the MRPs, the problems will need to be fixed before proceeding. Sellers and buyers should negotiate expenses. An appraisal also uses housing market data to see whether the proposed loan amount is comparable to that of similarly valued homes. Though the VA appraisal may seem tedious, it’s not much different than a standard appraisal. Homeowners who have maintained their home shouldn’t be too worried about major issues appearing.

Myth: VA Loans Can Only be Used Once

Luckily, the VA loan can be taken out multiple times as long as you have entitlement to use. Entitlement is how much the VA will guarantee the lender if you default. When you first use a VA loan, you have full entitlement. This means you can buy a home at any given price with no down payment, so long as your lender approves you for a mortgage. If you’ve fully paid off and sold your VA-financed home, your full entitlement is restored for your next purchase. It’s even possible to have more than one loan out at once if you use any remaining entitlement to buy another home. Be aware that if you’re buying with reduced entitlement, you’ll likely need a down payment.

The VA loan isn’t just a lucrative loan program, it’s a benefit you’ve earned through service. The intricacies of the loan have led to misunderstandings among military homebuyers and home sellers alike, which is why it’s crucial to work with a lender and real estate agent with a strong track record of working with VA homebuyers.

If you have any questions about the home buying process, contact one of our licensed Mortgage Loan Originators. If you are ready to buy a home, click here to get started!

For informational purposes only. You should refer to the VA for specific guidelines regarding your eligibility.

“Amortization” might sound complex and confusing, but it’s easy to understand once you know how it works.

What is Loan Amortization?

Amortization is when a loan’s balance is gradually reduced through routine payments. With an amortized loan (such as a mortgage), most of the initial loan payments will go towards the interest but will increasingly go towards the principal over time until the balance is zero. An amortized repayment structure makes becoming a homeowner more accessible and beneficial. Instead of having to pay back all the money you borrowed to buy a home in one large payment, amortization lets you pay off your mortgage in manageable chunks. Another perk is that with every principal payment, you’re increasing home equity and paying down your home faster. Making extra principal payments can help you pay off your mortgage early and save money in the long run; check that doing so will not result in prepayment penalties.

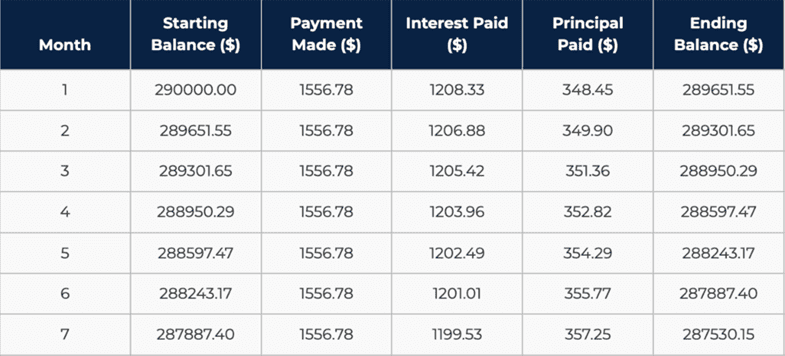

Mortgage Amortization: A Closer Look

If you were to get a 30-year fixed-rate mortgage of $290,000 at 5% interest, your monthly payment would be $1,556.78. In the first month, $1208.33 of that payment goes towards the interest, while only $348.45 is distributed to the principal. Each month afterward, a little bit more of the payment contributes to the principal.

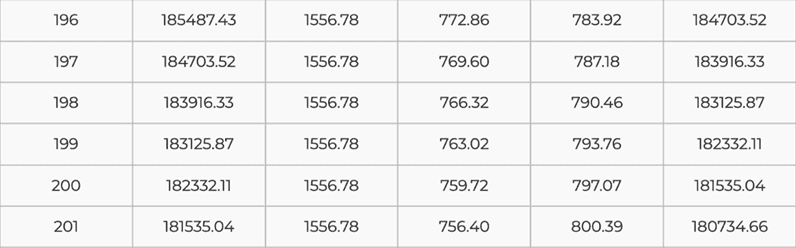

At 196 months, the portion that goes to your principal becomes greater than the interest portion, $783.92 versus $772.86, respectively. This shift continues for the rest of the 30-year loan term until the loan is paid off.

Most adjustable-rate mortgages (ARM) are amortizing, too. For hybrid ARMs where there’s an initial fixed-rate period, the loan follows a normal amortization schedule. Once the adjustable period begins, the loan will re-amortize each time the rate and monthly payment adjust. When you’re reviewing mortgage options with your Loan Originator, they’ll give you an amortization schedule so you can see the payment breakdown. You can also use an amortization calculator to get an estimate for a rough calculation.

Maintaining a mortgage is a massive financial responsibility, and it takes time to pay it off. When you understand how mortgage repayment is structured, you can make better financial decisions and feel confident that you’re breaking down your loan, one payment at a time.

If you want to know more about how to pay off your mortgage faster, contact one of our licensed Mortgage Loan Originators. If you are ready to begin the home buying process, click here to get started!