LINTHICUM, MD, March 20, 2023 – NFM Lending and its family of lenders have announced that they have earned the 2024 Top Workplaces USA award, issued by Energage, a purpose-driven organization that develops solutions to build and brand Top Workplaces. The Top Workplaces program has a 15-year history of surveying over 20 million employees and recognizing the top organizations across 60 markets for regional Top Workplaces awards.

Top Workplaces USA celebrates organizations with 150 or more employees that have built great cultures. Over 42,000 organizations were invited to participate in the survey. Winners of the Top Workplaces USA list are chosen based solely on employee feedback gathered through an employee engagement survey issued by Energage.

Results are calculated by comparing the survey’s research-based statements, including 15 Culture Drivers proven to predict high performance against industry benchmarks.

“Earning a Top Workplaces award is a badge of honor for companies, especially because it comes authentically from their employees,” said Eric Rubino, Energage CEO. “That’s something to be proud of. In today’s market, leaders must ensure they’re allowing employees to have a voice and be heard. That’s paramount. Top Workplaces do this, and it pays dividends.”

“We’re honored to be recognized as a 2024 Top Workplace by Energage and USA Today, reflecting our dedication to fostering a positive and inclusive culture,” said Stephanie L. Herring, Chief Human Resources Officer at NFM. “This achievement inspires us to continue prioritizing employee satisfaction and well-being as we strive for excellence.”

“This achievement would not have been possible without our incredible employees’ dedication and hard work,” said Bob Tyson, NFM President and Chief Operating Officer. “I want to thank them for their commitment to making the NFM Family of Lenders a truly great place to work.”

NFM Lending is a national mortgage lending company currently licensed in 49 states and Washington, D.C. The company was founded in Baltimore, Maryland in 1998. NFM Lending and its family of companies include Main Street Home Loans, BluPrint Home Loans, Elevate Home Loans, and Element Home Loans. They attribute their success in the mortgage industry to their steadfast commitment to customers and the community. For more information about NFM Lending, visit https://nfmlending.com/, like our Facebook page, or follow us on Instagram.

If you’re considering buying a home with an Accessory Dwelling Unit (ADU) or a property with ADU potential, or even adding one to your existing property, this is the article for you. Many Gen Z and millennial homebuyers are loving the idea of an Accessory Dwelling Unit to offset their mortgage with rental income through house-hacking. Other people may be interested in ADUs to gain extra living space for family, or with so many American’s working from home, added office space! There are tons of benefits to an Accessory Dwelling Unit and we’ll consider those and how you might go about owning one in this article.

What is an ADU?

ADUs are smaller secondary residential units on a single-family property. They typically feature a separate kitchen, bathroom, and entrance from the main house.

Types of Accessory Dwelling Units:

Apartment over garage

Garage conversion

Mother-in-law quarters

Backyard cottage

Granny flat

Prefab detached unit (Tiny home)

Who’s Building and Buying ADUs?

In today’s low-inventory housing market, ADUs are a great option for many people. Here are some reasons people build or buy properties with ADUs:

Expand living space: Create more space for family or extended family. Maybe a parent can live nearby with some privacy, or a grown child can return home without feeling cramped.

Downsize living: Move to a smaller space while staying on your property.

Home office or studio: Have a dedicated workspace conveniently located at home.

Offset mortgage or generate rental income: Some homeowners live in the main house and rent out the ADU to help pay the mortgage. Others choose to live in the ADU and rent out the main house.

Why are ADUs so Popular?

Making the Most of an ADU

ADUs are versatile spaces that can serve various purposes depending on your goals. Consider if you want more internal space (like a basement conversion) or more yard space. Do you aim for rental income? Maybe you want to downsize and live in the ADU while renting the main house?

Multigenerational Living: Many homeowners build ADUs for aging parents or adult children who need a place to live. ADUs offer privacy and independence while keeping loved ones close.

Rental Opportunities: With high housing demand, building an ADU for real estate investment can provide a steady income stream. Whether you choose long-term tenants or short-term vacation rentals, an ADU can help offset your mortgage or provide extra cash flow.

Short-Term Rentals and Airbnb: Especially in tourist areas, short-term rentals are a popular option for ADU owners. Listing your ADU on platforms like Airbnb allows you to tap into a growing market for unique accommodations. Short-term rentals offer flexibility and potentially higher rental rates during peak seasons. However, be sure to check local regulations and HOA rules regarding short-term rentals before pursuing this option.

Home Office or Workspace: If you work from home or need a dedicated space for hobbies, an ADU can be the perfect solution. Design the space to meet your specific needs and enjoy a separate area to focus on work or passions.

Guest Accommodations: An ADU can also function as a comfortable and private space for guests. Whether you have out-of-town friends or family visiting or want to offer a unique Airbnb experience, an ADU provides a welcoming place for guests to stay.

Does an ADU Add Value to Your Home?

Home improvement projects like kitchen updates, bathroom additions, and energy-efficient windows can increase your home’s value. Building an ADU is another great way to add value.

ADUs can be profitable in smaller cities and towns as well as urban areas, but provide another great benefit of affordable housing in places where it is highly sought after. A study from Porch showed that in large cities, properties with ADUs typically sell for 35% more than similar homes without them.

Increased Property Value and Rental Income Potential

Property Value: Constructing an ADU on your property typically increases the resale value of the property. An appraiser will consider the value of other homes with ADUs when appraising yours. Properties with ADUs often sell for a premium because they offer an income-producing unit and more total living space.

Rental Income: In addition to the added value of increased property value, ADUs can provide a steady stream of rental income, helping offset mortgage payments or providing extra cash flow. They can also offer more privacy than simply renting out a room in your main house.

Are There Downsides to an ADU?

There can be a few drawbacks to consider depending on the type of ADU you have, how you use it, and your expectations going in:

Space Limitations: ADUs are inherently smaller spaces, which may not be ideal for everyone.

Construction Costs: Building an ADU can be expensive, especially if it includes a kitchen, bathroom, and separate entrance.

Building and Zoning Regulations: There are zoning regulations and permitting processes to navigate when building an ADU.

Privacy Concerns: Depending on the layout of your property and ADU, there may be some privacy considerations for both you and your tenants.

Maintenance and Upkeep: Like any additional structure, an ADU requires maintenance and upkeep.

Does Adding an Accessory Dwelling Unit Increase Property Taxes?

Adding an ADU may increase your property taxes because it increases the value of your property. It’s recommended to reach out to your county assessor’s office beforehand to determine the potential tax impact. Consulting with an accountant or tax advisor can also be beneficial to discuss your specific situation.

Can an ADU Have a Separate Address?

Whether or not an ADU can have a separate address depends on your location. Here are some possibilities:

Half address or unit designation: Some homeowners use a ½ address or add “Unit B” or “Unit 2” to the existing main address.

Assigned address during permitting: In some states, an ADU is assigned an address during the building permitting process.

No separate address: In other states, the ADU may not be assigned a separate address.

ADU Zoning, Rules, and Regulations

Importance of Early Planning

Thinking about building an ADU requires early preparation for a smooth process. Zoning regulations and legal requirements are in place to ensure these projects align with the community’s planning goals. Cities and counties have varying approaches to ADUs; Some actively encourage them for more housing options, while others have restrictions to protect existing neighborhoods. Understanding the specific rules in your desired location is crucial. Don’t assume what’s allowed elsewhere applies to your area!

Contact your local planning department. They are the ultimate authority on what you can and cannot build. Proactive research pays off. Before investing in design plans, consult the planning department to understand restrictions like minimum lot size, height limitations, allowable square footage, and any parking requirements. Some cities even have pre-approved ADU designs to streamline the process!

Partner with experienced professionals. Architects and builders well-versed in ADU construction are invaluable. They understand the nuances of the permitting process and can translate zoning code legalese into practical advice for your project. Their knowledge of local regulations can even help you explore creative design solutions that maximize your project’s potential while remaining fully compliant.

Working with Professionals: Contractors and Designers

To ensure your ADU meets all requirements and integrates seamlessly with your property, working with experienced contractors and designers specializing in ADU construction is essential. Here are some qualities to look for in professionals:

Licensed and insured

Experience building ADUs

Provide references and examples of their work

Understand local zoning laws and permitting requirements

Which Loan Types Allow for ADUs?

Financing an Accessory Dwelling Unit can vary depending on how you plan to use it. If you intend to use rental income from the ADU to offset your mortgage or qualify for a larger loan, many loan types will allow for current or projected rental income to be taken into consideration, while others don’t.

Loans That Allow Rental Income from ADUs

Conventional Loans: A conventional loan is any mortgage loan that is not insured or guaranteed by the government (such as under Federal Housing Administration (FHA), Department of Veterans Affairs (VA), or US Department of Agriculture (USDA) loan programs).

FHA Loans: The Federal Housing Administration (FHA) now allows homebuyers to use projected rental income from ADUs to qualify for mortgages on new construction, homes with existing ADUs, or renovations that include ADUs. Learn more about the new FHA financing policies as of 2023.

VA Loans: VA loans are offered by the Department of Veterans Affairs to help servicemembers, veterans, and their families buy homes.

Construction Loans: build a brand new home and include an ADU in the plans

Renovation Loans: From Fannie Mae HomeStyle, Freddie Mac Choice Renovation and FHA 203(k) a renovation loan can act as a bridge between what a property is now, and what it could be with a bit of extra work.

Loans You Can’t Use Rental Income from ADUs to Qualify

USDA Loans: If you’re looking to buy a home outside of a big city, with no down payment, a USDA home loan is a great option. However, you cannot use rental income from an Accessory Dwelling Unit on the property to qualify for the mortgage. With a USDA loan, you would be better off using the ADU for single-family living, multigenerational living situations, or an office/additional space for those residing in the main unit.

Considering the Next Steps with an ADU

If you’re interested in exploring the possibility of adding an Accessory Dwelling Unit to a property you’d like to buy, or purchasing a property with an Accessory Dwelling Unit already onsite, here are some next steps:

Get Preapproved! As a home mortgage lender near you, I’m excited to explore if buying a property with an ADU, or building onto an existing property is right for your goals. Together we can determine the budget for your plan and we can guide you through your next steps. We’ll also discuss which loan options are available to you based on your financial situation and how you plan to use the ADU.

Talk to an Agent. If you haven’t yet talked to a real estate agent, we are happy to provide a recommendation. Someone who is experienced in buying or selling income producing properties including ADUs will have a ton of knowledge and info to give you. They can guide you around potential pitfalls before you even start searching for the right property.

Research local zoning regulations and permitting processes. Contact your local planning department to learn about the specific requirements in your area.

Consult with a qualified architect or builder experienced in ADU construction. They can help you assess the feasibility of your project and navigate the design and permitting process.

By carefully considering these factors and taking the necessary steps, you can determine if an Accessory Dwelling Unit is the right fit for you and unlock the potential value and functionality it can add to your current or future property.

If you’re in the market for a new home, you’re probably keeping an eye on the current interest rates. When rates are low, it can be easier to jump into the homebuying process, but not so much when rates are high. Fortunately, if you’re ready to buy a home now, there’s something you may be able to do to pave the way for more manageable mortgage payments, regardless of what the market is up to. One of these handy strategies is called a Temporary Buydown.

Explaining Temporary Buydown Mortgages

A Temporary Buydown is an option where a buyer is able to temporarily reduce the interestrate on their new loan, in exchange for a one-time fee at closing. This tactic can give a homebuyer some breathing room and help ease into the full mortgage payment through the first few years of the loan, especially in a high interest rate environment.

How does a Temporary Buydown Work?

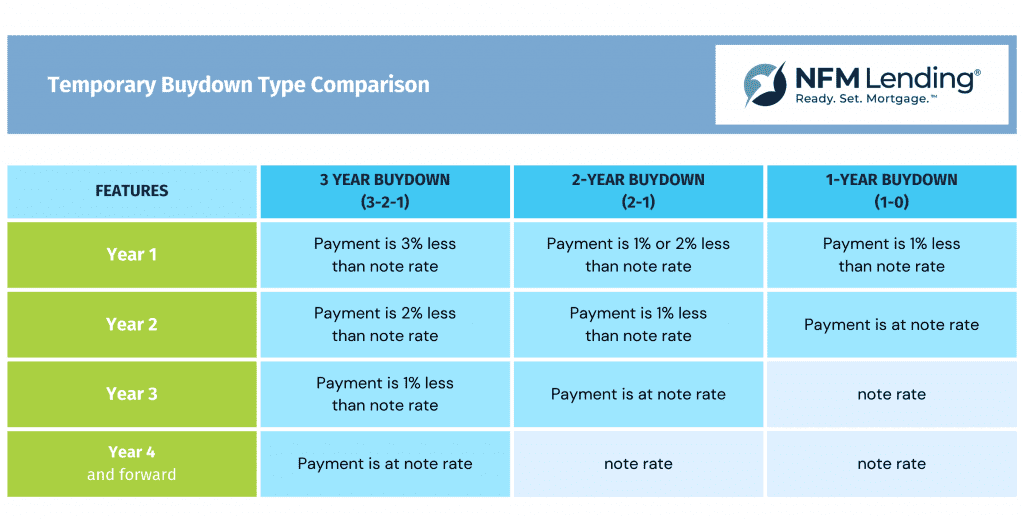

There are different buydown options, each offering a specific reduction in interest rate for a set period.

At NFM, we offer three different types of temporary buydowns:

1 Year Buydown (1-0 ): This option allows for the effective rate of interest paid by the buyer to decrease by 1% for the first year of the mortgage loan.

2 Year Buydown (2-1): The option allows for the effective rate of interest paid by the buyer to decrease by 2% for the first year of the mortgage loan and 1% for the second year.

3 Year Buydown (3-2-1): This option allows for the effective rate of interest paid by the buyer to decrease by 3% for the first year of the mortgage loan, 2% for the second year and 1% for the third year.

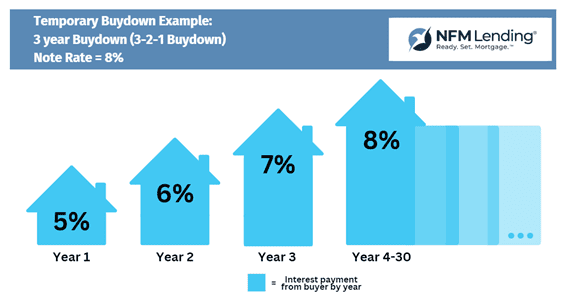

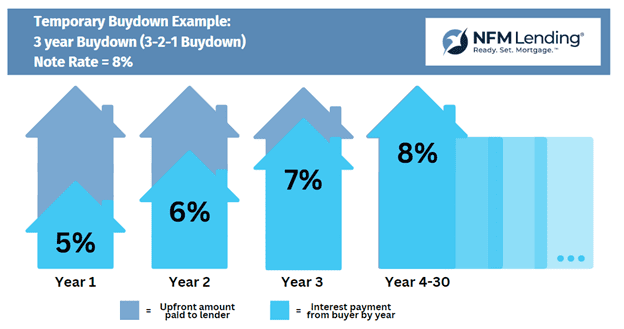

Temporary Buydown Example

Let’s say you secure an 8% interest rate on a 30-year fixed-rate mortgage with a 3 year buydown (3-2-1 buydown).

Year 1: Your payment will be based on a 5% interest rate (8% – 3% = 5%).

Year 2: You’ll make payments calculated at a 6% interest rate (8% – 2% = 6%).

Year 3: Your payments reflect a 7% interest rate (8% – 1% = 7%).

Year 4 onwards: Your monthly payments transition to the original 8% interest rate for the remaining loan term.

So, for as long as you own the home, or until you refinance to a new loan with a potentially lower interest rate, you will continue to make the principal and interest payment based on this 8% rate.

Temporary Buydown Calculator

Use our temporary buydown calculator to estimate the cost and potential savings associated with different buydown scenarios. We can also discuss if this makes financial sense for you any time!

Who Pays for a Temporary Buydown?

There are several ways to fund a temporary buydown:

Seller/Builder Concession: Traditionally, sellers or builders will offer a temporary buydown as a seller concession to attract buyers, especially in a slow market.

Buyer Funded Buydown: You can choose to pay for the buydown yourself at closing. This might be a good option if you have the savings and want to lock in lower monthly payments in the early years of your loan.

Lender or Realtor Incentive: In some cases, lenders or real estate agents may offer a temporary buydown as part of a promotional package.

Funding and Cost Considerations

The party responsible for paying for the buydown pays the amount as a closing cost when the loan is funded. The amount is equal to the buyers interest savings. Meaning the difference between the final note rate and the agreed lower interest rate during the first years of the loan.

These funds are deposited into a custodial escrow account at closing. The loan servicer then draws from the account every month to make up the difference between the full loan payment and the discounted bill the homeowner is paying.

Temporary VS Permanent Buydown

While both options involve lowering your interest rate, temporary and permanent buydowns have key differences:

Reduction Amount: Temporary buydowns offer a more significant initial reduction (up to 3%) compared to permanent buydowns (typically 0.125% – 0.5%).

Loan Structure: Temporary buydown funds are held in an escrow account and used to supplement your monthly payments. In a permanent buydown, the lender reduces the loan amount itself.

Buyer Qualification: For a temporary buydown, you need to qualify for the full loan amount and original interest rate even though you’ll pay lower rates initially. Conversely, you only need to qualify for the reduced interest rate with a permanent buydown.

When is the best time to use a Temporary Buydown?

Temporary buydowns can be a good idea for first-time home buyers who are shocked by the speed at which mortgage rates have risen, and who will deplete their savings on the down payment and closing costs. The temporary payment reduction allows borrowers to replenish savings or spend the money on home upgrades.

The most favorable time to take advantage of a buydown is when the seller or builder is offering to contribute cash towards closing. Sometimes this can happen as an incentive to get a buyer to purchase their home or to encourage the purchase of a home in a newly built community. If this isn’t an option, a buyer can often still pay down the rate themselves.

Final Thoughts

Now that you understand temporary buydowns, it’s crucial to weigh the pros and cons against your individual financial situation and homebuying goals. Consulting with a mortgage professional is the best way to determine if a temporary buydown aligns with your needs. They can assess your eligibility, calculate potential costs and savings, and guide you through the entire mortgage process.

Beyond temporary buydowns, there are other strategies to navigate the homebuying journey in today’s market. Our team of home loan experts is dedicated to helping you explore all your options. Additionally, check out our blog for informative articles on various mortgage programs, down payment assistance, and tips for first-time homebuyers.

Let us empower you to make informed decisions and turn your dream of homeownership into reality. Contact us today to schedule a free consultation!

*Reduction in payment is the result of builder or seller concessions used to buy down the rate and are not guaranteed by NFM Lending. 5% down payment is the responsibility of the borrower. Available for fixed-rate conventional, VA, USDA, and FHA loans. For new or existing home purchases only.

We love helping Gen Z and millennials navigate the exciting world of homeownership. Let’s face it, between inflation, student loans, monthly bills and trying to go on vacation someday, saving for a down payment can feel like climbing Mount Everest in flip-flops. But what if there was a way to hack the system, own a piece of real estate and potentially live for free (or close to it)? Buckle up, because we’re diving into the world of house hacking strategies.

What is House Hacking?

Imagine this: you buy a nice duplex in a good area with two separate units. You live on one side, rent out the other, and – plot twist – that rent covers most, if not all, of your mortgage payment. That’s the magic of house hacking! It’s all about buying a multi-unit property (think duplexes, triplexes, or fourplexes) or a single-family home with a rentable space (like a finished basement or in-law suite). You live in one unit and rent out the others, turning your home into an income stream.

Benefits of House Hacking:

With so many young adults hoping to buy homes, and rent prices are brutal these days and house hacking offers a way to save money on your living expenses. Ideally, your rental income covers most of your mortgage payment, property taxes, and insurance (PITI). That translates to living for free (or very cheap) while building equity in your property – a major win-win!

But house hacking goes beyond just saving money. It’s a springboard for ambitious young adults or anyone interested in financial independence. Here’s how:

Jumpstart Your Investment Journey: House hacking gives you valuable real estate experience. You learn the ropes of being a landlord, from screening tenants to managing minor repairs. This knowledge becomes a steppingstone for future real estate investments, allowing you to build wealth and diversify your income streams. It’s often said that the average millionaire has around 7 income streams. So, add rental income to your other income stream(s) and you’re one step closer to retirement!

Build Equity While You Live: Remember that house you’re living in? As you make mortgage payments and property values hopefully increase, you’re building equity – essentially ownership – in your property. This equity can be tapped into down the line for various purposes, like a bigger investment property, upgrading with renovations to your current property/properties, or even paying down consumer or student debts.

Become a Mini-Landlord Boss: House hacking equips you with valuable life skills. You’ll learn business budgeting basics to manage your property’s finances, hone your people skills when screening tenants, and even develop some DIY prowess for minor maintenance tasks.

House Hacking Strategies:

House hacking isn’t a one-size-fits-all strategy. The beauty lies in its flexibility. Here are some popular house hacking approaches to consider:

House Hacking with Roommates

Maybe you’re not quite ready to jump into managing a separate unit. House hacking with roommates is a fantastic way to test the waters. Here’s the idea: you find a single-family home with extra bedrooms and share it with responsible roommates. Their rent contribution significantly reduces your monthly housing costs, freeing up cash for other goals.

Pro Tip: When screening roommates, prioritize responsible individuals who align with your lifestyle. Open communication and clear house rules are key to a harmonious co-living experience.

Hacking a Multi-Unit Property

Ready to dive deeper? Look into multi-unit properties like duplexes, triplexes, or even fourplexes. These properties offer dedicated rental units that provide a more consistent and potentially higher rental income compared to roommates. Live in one unit, rent out the others, and watch your rental income potentially cover a significant chunk of your mortgage payment.

Things to Consider: Multi-unit properties come with additional responsibilities like managing separate entrances and potentially maintaining shared yards. Make sure you’re comfortable with the extra workload before taking the plunge.

House Hacking with an ADU

Does your dream home have a finished basement or a separate in-law suite? An Accessory Dwelling Unit (ADU) could be your perfect house hacking setup. You could rent out the additional space for a steady income stream while still enjoying the privacy of your main living area.

Keep in Mind: Pay attention to local zoning and permit regulations for specific requirements for renting out any type of ADU. Do your research and ensure your property complies with all the rules before advertising the space. Your friendly real estate agent should be able to help you understand your local limitations (let us know if you’d like us to connect you with someone we trust!)

Getting Started with House Hacking:

House hacking might sound complex, but with the right guidance, it can be a smooth and rewarding experience. Here’s how we can help you navigate the house hacking journey:

The Financials:

Loan Options: The absolute best part (in our opinion) of house hacking is that these homes can be purchased with a traditional mortgage (think FHA, VA, USDA and Conventional loans) with more competitive interest rates, depending on your credit score and financial situation than if you were to purchase an investment property separate from your primary residence.

Down Payment Assistance: There are fantastic programs available to help first-time homebuyers with their down payment. We’ll explore these options and see if you qualify for any additional down payment assistance programs.

Affordability Calculations: House hacking isn’t just about finding a cool property. We’ll do a deep dive into your finances to ensure you’re comfortable with the ongoing costs of ownership, including property taxes, insurance, and potential maintenance needs. We’ll also factor in projected rental income to create a realistic picture of your monthly expenses.

Building Your Dream Team:

House hacking doesn’t have to be a solo act. Here’s how I can help you assemble your dream team:

Realtor: A good realtor is your partner in crime when it comes to finding the perfect house hack property. If you aren’t already working with someone, we have trusted, experienced partners we can connect you with who understand the house hacking market and can guide you through the buying process.

Property Management (Optional): If managing tenants seems daunting, consider partnering with a reputable property management company. They can handle everything from tenant screening and rent collection to maintenance requests and repairs, freeing up your time and minimizing stress.

Lawyer: When contracts are involved, it’s always a wise decision to lawyer up and make sure your lease or rental agreement is rock solid. You don’t want to take on the financial burden of someone else’s mistakes if it can be helped.

Finding the Right Property:

Location, Location, Location: Just like any real estate investment, location is key. Discuss with your real estate agent neighborhoods that have a high rental demand and good potential for stable tenant occupancy.

Rental Potential: Not all properties are created equal for house hacking; analyze factors like the number of bedrooms and bathrooms in the rentable units, overall square footage, and amenities that might attract tenants and command higher rent.

Property Types: It’s obvious to say that different house hacking strategies require different property types. Whether it’s a multi-unit property with separate entrances or a single-family home with a rentable basement, all of that will be covered while you work with your homebuying team.

Conclusion:

House hacking isn’t for everyone. It requires some upfront effort, financial responsibility, and a willingness to learn. But for ambitious go-getters, who are ready to take control of their financial future, house hacking can be a game-changer. It allows you to live for free (or close to it), build equity, gain valuable real estate experience, and potentially set yourself on a path to financial freedom.

Ready to chat? Let’s schedule a consultation to discuss your financial goals and see if house hacking aligns with your vision.

LINTHICUM, MD, January 2, 2024 – NFM Lending is honored to have been named a Top Workplace by Scotsman Guide for 2024. This is Scotsman Guide’s inaugural year hosting the award and the first time NFM has won it. According to Scotsman Guide, a Top Workplace is a company that has exceptional achievements in operations, benefits, corporate culture, philanthropy, and DEI commitment. Although the Top Workplaces feature is not a ranking like Scotsman Guide’s other awards, NFM Lending was included in the Editor’s Picks category along with 15 other companies.

“We are immensely honored to be named a ‘Top Workplaces 2024’ by Scotsman Guide, a testament to our unwavering commitment to fostering a workplace culture that values excellence, collaboration, and innovation,” said Gene DiPaula, Vice President of Communication at NFM. “This recognition reflects every team member’s dedication and hard work, and we are proud to be acknowledged by the leading resource for mortgage loan originators. As we continue to prioritize a thriving work environment, this accolade inspires us to reach even greater heights in delivering outstanding service to our customers and cultivating a workplace where success is celebrated together.”

The company and its loan originators have received numerous accolades from Scotsman Guide over the years for excellence in lending and record sales numbers. NFM has made the Top Mortgage Lenders list for five years and is among the top 30 lenders nationwide.

NFM Lending is proud of this new recognition and is thankful to everyone in the NFM Family of Lenders for their contributions.

About NFM Lending

NFM Lending is a national mortgage lending company currently licensed in 49 states in the U.S. and Washington, D.C. The company was founded in Baltimore, Maryland in 1998. NFM Lending and its family of companies includes Main Street Home Loans, BluPrint Home Loans, Elevate Home Loans, and Element Home Loans. They attribute their success in the mortgage industry to their steadfast commitment to customers and the community. For more information about NFM Lending, visit www.nfmlending.com, like our Facebook page, or follow us on Instagram.

If you’ve been eyeing interest rates and waiting for an opportunity to refinance, your time has come! Refinancing is an excellent way to make your home work for you, and we’re answering the top five questions people have about refinancing.

How does refinancing work?

Refinancing is when your original loan is replaced with a new loan with different terms. It can be a smart move if you plan to stay in your home for a while; use a refinance mortgage calculator and speak with a lender to know your breakeven point. Many people refinance to lower their monthly payment, but it can also be used to access home equity, remove someone from the mortgage, get rid of private mortgage insurance (PMI), or change your loan type. Work with a loan originator to find out what refinance option is right for your needs.

What kinds of refinances are there?

Much like purchase loans, there’s no one-size-fits-all refinance. There are several types of refinances that can help you achieve your financial goals:

Rate and term refinance: This is the most common type of refinance because it allows you to lower your monthly payment or shorten the loan’s term. When interest rates drop, it’s a great time to take advantage of a rate and term refi, especially if you bought your home at a higher rate. You can also use this type of refinance to change your loan type (like going from an adjustable-rate to a fixed-rate mortgage) or remove PMI. Be aware that lowering your payment can lead to a longer term and more payments for the life of the loan, while choosing to shorten the repayment period can lead to a higher monthly payment.

Cash-out refi: A cash-out refinance leverages your existing home equity by replacing your first loan with a higher mortgage and giving you the difference in cash. There’s no limit to how you can use your newfound funds—they can be used to pay off debt, make home repairs, take a vacation, or to pay for tuition. Since a cash-out refinance is riskier, the rates can be slightly higher than other refinance types. Cash-out refinances are also available for VA and FHA loans. You’ve put so much love and labor into your home, and a cash-out refi lets you reap those rewards!

Streamline or Interest Rate Reduction Refinance (IRRRL): A streamline refinance could be a good option for you if you have a FHA, USDA, or VA loan. Streamlined refinances and IRRRLs reduce how many items (such as an appraisal or credit check) are needed for eligibility, shortening the process.

Renovation Loans: The Fannie Mae Homestyle Renovation Loan, FHA 203(k), and VA Renovation are specifically for people who want to make home repairs or upgrades. One benefit of these options is that the renovation costs are rolled into the new loan amount, so there’s only one closing and one interest rate. Instead of using your home’s current value for the loan amount, your lender will use the detailed project proposal submitted by your contractor to determine your home’s “as-completed” appraised value.

Additionally, some lenders offer incentives that allow you to refinance with little-to-no fees when rates drop, making refinancing even more attractive.

When can I refinance my home?

Depending on the refinance program you choose, there may be a minimum requirement for the number of payments made or length of homeownership, though this is more often the case for loans backed by the federal government. Some conventional loans don’t have a wait time, but cash-out refis usually have a six-month waiting period. Wait times vary depending on your lender, your current mortgage, and your refinance plan. Your current equity is also a major determining factor. For example, 20% in home equity is required for most cash-out transactions. There’s also no limit to how many times you can refinance the same property if you meet eligibility requirements.

Are there closing costs?

Even though you already own your home, you may be surprised to know there can be closing costs when refinancing. Closing costs can be 2-5% of the loan amount, though this can vary. Much like the closing costs associated with buying a home, the fees for a refinance may include an origination fee, recording fee, appraisal fee, and more. Note that some refinances require an additional fee in addition to closing costs: the FHA Streamline refinances come with a mortgage insurance premium (MIP) and an upfront mortgage insurance premium (UFMIP); VA Streamline refinances mandate a funding fee of 0.5% for most cases.

How long does it take to refinance?

On average, it takes 30 days to refinance a home. The process is similar to buying a home in it involves submitting an application, providing any needed documents, going through a home appraisal in (some instances), getting underwriting approval, and attending closing. Sending correct information to your lending team on time will go a long way in speeding up the process.

No matter your reason for refinancing, it’s important to understand your goals and what’s involved with the process. Working with an experienced lending team will ensure your refi goes smoothly.

For informational purposes only. Refinancing an existing loan may result in the total finance charges being higher over the life of the loan. Veterans Affairs loans require a funding fee, which is based on various loan characteristics. LTVs can be as high as 96.5% for FHA loans. FHA minimum FICO score required. Fixed-rate loans only. W2 transcript option not permitted. Minimum required credit score of 620 for conventional loans.

LINTHICUM, MD, November 15, 2023 — NFM Lending is pleased to announce the opening of a new branch led by Branch Manager Kenneth Ufret. Pending licensing finalizations, the branch will be located in Cherry Hill, NJ. The NFM Lending branch will focus on expanding NFM’s flexible and powerful lending platform to better serve community families with exceptional customer service. NFM Lending offers Conventional, FHA, VA, USDA, FNMA, Jumbo, and many other loan options to fit every borrower’s needs.

The branch’s goal is to continue to provide the same commitment and dedication to borrowers, ranging from first-time homebuyers to seasoned buyers looking for their next home, a second home, or investment properties.

“In this changing market, I went with a company that has the products and programs needed to meet any buyer’s needs, along with a reputation for superior customer service,” said Ufret.

“We are very excited to have Ken join our team in the Philadelphia market,” said Branch Manager Jeffrey Rice. “Ken brings over 30 years of experience in real estate and mortgage financing, and he is a well-respected and proven leader in the community. Ken will us help grow NFM in the Philadelphia area in the years to come.”

Ufret is currently seeking qualified Mortgage Loan Originators for full and part-time positions.

NFM Lending is a national mortgage lending company currently licensed in 49 states and Washington, D.C. The company was founded in Baltimore, Maryland in 1998. NFM Lending and its family of companies includes Main Street Home Loans, BluPrint Home Loans, Elevate Home Loans, and Element Home Loans. They attribute their success in the mortgage industry to their steadfast commitment to customers and the community. For more information about NFM Lending, visit www.nfmlending.com, like our Facebook page, or follow us on Instagram.

LINTHICUM, MD—December 12, 2023— NFM Lending is proud to announce it was named a Top Workplace by The Baltimore Sun. NFM Lending has received this honor for twelve consecutive years. The publication held the Top Workplaces awards ceremony on December 7, 2023, at the Grand Lodge of Maryland in Hunt Valley, MD.

Out of 155 Baltimore-area businesses, NFM Lending ranked #10 for companies with 150-399 employees. Each year, the Baltimore Sun distributes a survey to employees of Baltimore area workplaces. The survey analyzes job satisfaction and engagement of employees along with the values and organizational health of the company.

“We are immensely honored to be recognized as a ‘Top Workplace’ by the Baltimore Sun,” said NFM President and Chief Operating Officer Bob Tyson. “This accolade is a testament to the exceptional dedication and talent of our incredible team at the NFM Family of Lenders. Our success is a direct result of the hard work and commitment of each employee, who consistently contributes to our vibrant and positive workplace culture. We take great pride in fostering an environment where innovation, collaboration, and excellence thrive. This achievement is a reflection of our collective efforts, and we remain committed to maintaining a workplace that empowers and inspires every member of our NFM family.”

NFM Lending prides itself on its exceptional culture. The company fills the employees’ work environment with encouragement and teamwork, building a positive workplace that rewards commitment and performance. Management encourages employees to voice their questions and concerns, which are addressed promptly and appropriately. In addition, managers often surprise staff members for their birthdays, and the company holds contests, holiday celebrations, and other initiatives to encourage collaboration and show employees their appreciation.

NFM Lending is consistently recognized for its exceptional company culture. These awards include Top Workplace USA by Top Workplaces and Energage, Top Mortgage Employer by National Mortgage Professional Magazine; Top Workplace by the Washington Post; and ‘Best Mortgage Companies to Work For’ by National Mortgage News. NFM Lending is proud of these accomplishments and its team’s work to make it a Top Workplace.

About NFM Lending

NFM Lending is a mortgage lending company currently licensed in 49 states and Washington, D.C. The company was founded in Baltimore, Maryland in 1998. NFM Lending and its family of companies includes Main Street Home Loans, BluPrint Home Loans, Elevate Home Loans, and Element Home Loans. They attribute their success in the mortgage industry to their steadfast commitment to customers and the community. For more information about NFM Lending, visit www.nfmlending.com, like our Facebook page, or follow us on Instagram.

With the oldest turning 26 this year, most Gen Z’ers aren’t quite ready for homeownership — but a burgeoning set of this young generation plans to buy in the next few months, NFM Lending found.

How can lenders target and capture the latter? We can sum up the most effective strategy with one word: Influencers.

In the last decade, social media influencers revolutionized how companies reach their target audiences. In return, this spawned a new generation of consumers who are too savvy for traditional marketing methods.

Gen Z’ers view their favorite content creators as trusted peers and expect products to be authentic and personalized to their individual needs. They prefer to receive information through videos, on apps like YouTube and TikTok.

Sixty percent of the app’s users are Gen Z, providing a well-stocked pool of potential new loan applicants. To tap into it, NFM Lending launched an in-house influencer division in January 2022, led in part by Scott Betley, otherwise known as @ThatMortgageGuy on TikTok, Instagram, Facebook and YouTube.

In just a year and a half since, NFM Lending expanded to 16 in-house influencers, creating increasingly popular informative and entertaining videos.

Betley grew his fanbase to more than 1 million followers across all platforms as of this post’s publish date as a testament to their efficacy. He’s clocked more than 10 million views to his most popular videos — several of which compare the plight of Gen Z’ers saving for down payments to Boomers enjoying homes they bought affordably in the 1980s.

One of the talented creators recruited for NFM’s in-house influencer team is Jordan Nutter, aka @ANutterHomeLoan, whose satirical yet educational posts elicit genuine belly laughs. Jordan has over 240k followers across all platforms and hundreds of thousands of views on her videos. She is best known for her phone call reenactments inspired by real-life conversations with her clients. Jordan has immersed herself in the division’s success and was promoted to become its Vice President earlier this year.

How does NFM’s strategy stand out from other mortgage companies? NFM Lending takes its strategy a step further than its competitors. When visiting an influencer’s profile, users are guided to an optional intake form where they can share their financial statuses, contact information and how soon they plan to buy.

“It’s the roadmap to their homebuying journey,” NFM Lending Managing Director Gregory Sher explains. “The ‘Timeframe to Purchase’ field sets the clock in motion and allows us to create workflows to help the consumer accomplish their goal.”

NFM Lending’s clever method is the mouth of a funnel that narrows as it nurtures users deeper into the mortgage landscape. From 30.7 million TikTok views from Gen Z users in July 2023 (up 21.8% from June), NFM Influencers generated 1,401 leads. These became 24 prequalification applications and, finally, 20 loan originations. Of these leads, 941 asked for a real estate agent introduction.

Beyond creating leads and loan applications, the intake form provides data sets that offer unique insights into the behaviors and circumstances of Gen Z homebuyers.

Based on the numbers collected between July 2021 and 2023, we learned that:

Nearly all Gen Z respondents currently rent and plan to own

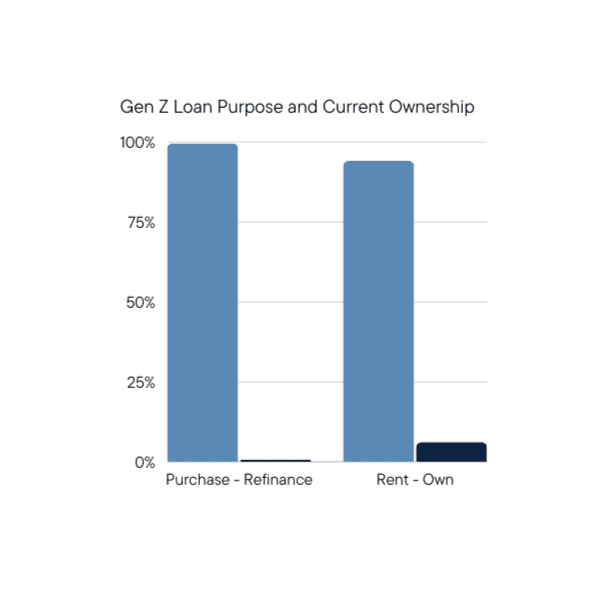

NFM Lending data confirms that most of this younger generation is headed toward homeownership for the first time. Of the 2,191 Gen Z’ers who shared their current ownership through our intake form in that timeframe, 93.9% were renters. Similarly, 99.4% of 2,575 said they’d use their mortgages to buy homes, rather than to refinance or build.

But with rents at record highs, we’re in a historically difficult time for renters to save for down payments. In July 2023, the national median rent was $2,038, which equals a whopping 75% of Gen Z’s median income of $32,500. That makes it especially tough for them to set aside piles of cash, but to put 20% down for the median U.S. home price of $416,100, they’d need to stack up $83,220.

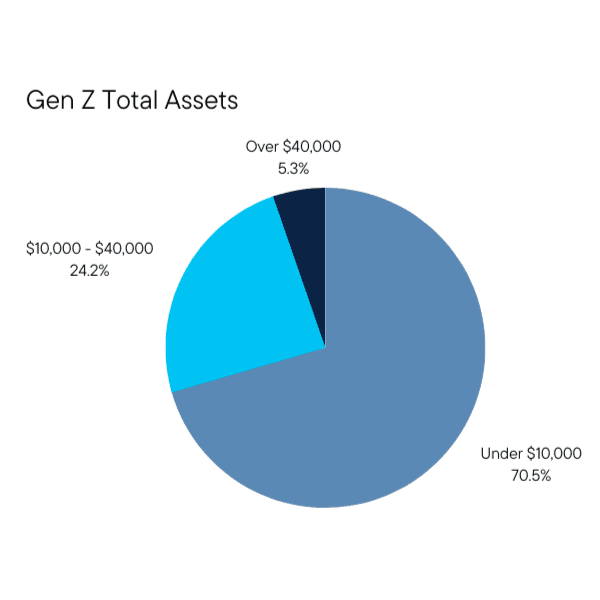

Of 922 respondents who revealed the value of their assets, including savings, to NFM Lending, just 5.3% had more than $40,000. Most had less than $10,000 (70.5%) and the rest had $10,000-$40,000 (24.2%).

Fortunately, down payment assistance programs can help, as can mortgage products that require less than 20% down. Take, for example, the NFM Zero Down Flex, which has no income cap and offers 100% financing for conventional loans.

And as Gen Z learns to navigate their unique circumstances, a burgeoning set is ready to buy.

One-third of Gen Z respondents expect to buy in 3-6 months

While 87% of respondents to a Gen Z Planet study said they’d love to own homes one day, the dream feels out of reach for many. A Freddie Mac survey found that 34% of Gen Z’ers worry they’ll never afford to buy places of their own, with insufficient credit history, lack of stable income and student loan debt cited as their primary obstacles.

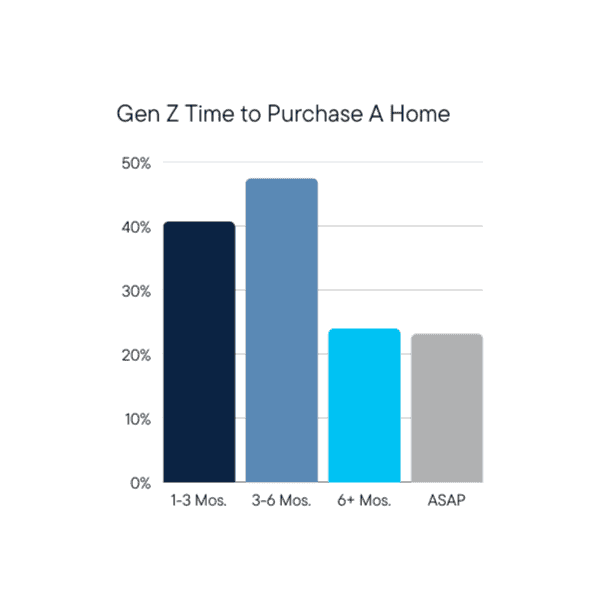

And yet, of the 1,920 Gen Z’ers who shared with NFM Lending how soon they plan to buy homes:

27.1% said they expect to in 3-6 months

25.9% selected 1-3 months

23.9% responded 6+ months

23.1% put ASAP

Altogether, 53% of the Gen Z TikTok users who offered their information to NFM Lending planned to buy homes within six months. But does that mean their incomes qualify for mortgage loans? Our data is promising.

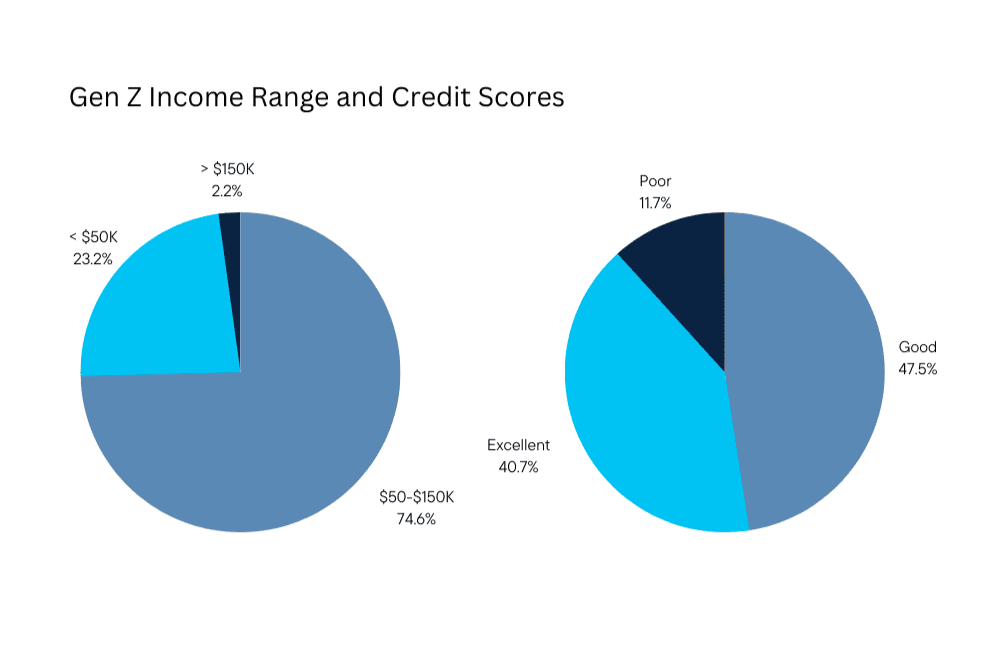

Nearly 75% of Gen Z respondents earn $50,000-$150,000

NFM Lending found that most Gen Z respondents made enough money to satisfy lender requirements. Of the 858 respondents who shared their incomes:

74.6% had an annual household income of $50,000-$150,000

23.2% earned less than $50,000

2.2% made more than $150,000

In terms of credit, of 1,129 respondents, 40.7% said they had an Excellent score, while 47.4% reported a Good one. And though nearly 12% admitted to having a low score, data showed that was more likely due to their lack of credit than being irresponsible with payments.

“In other words, they need more open trade lines such as credit cards that show a good pay history,” Sher says.

Being that they’re just setting off in their adulthood, it’s understandable that Gen Z’ers need some guidance while establishing themselves financially.

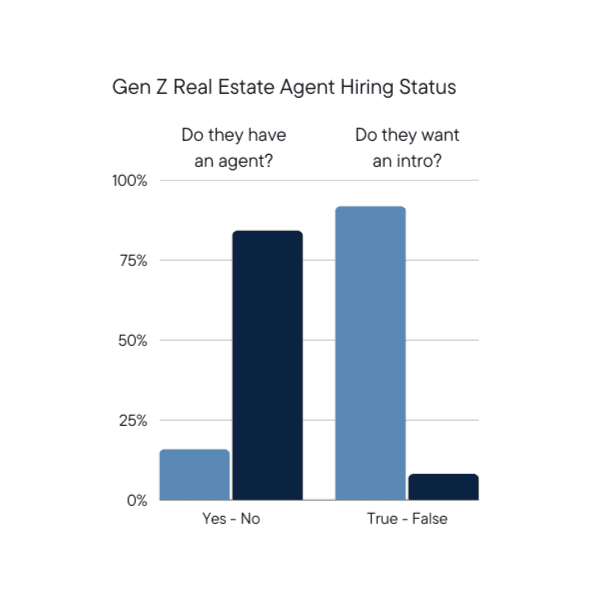

91.8% of Gen Z respondents asked for a real estate agent introduction

As first-time homebuyers, this young generation could use assistance navigating the housing market.

Traditionally, the path to homeownership involved finding a real estate agent who recommended a lender from their carefully curated Rolodex. Lately, however, that sequence started to flip. Many homebuyers today start off by shopping for a lender to see which loans they qualify for.

Through its intake form, NFM Lending reaches buyers in the infancy stage of their journeys, long before they’re ready to meet with a real estate agent. Of the respondents who shared their status of hiring a pro for their search, 84.1% of 2,178 said they didn’t yet have an agent and 91.8% of 756 respondents welcomed an introduction to one.

This change in the process allows loan officers to send prepped homebuyers to real estate agents with warm handoffs. They can source their personal directories and the roster of talented folks at Clever Real Estate, an NFM Lending partner, to suggest the pro that might work best with each buyer.

However, it also gives loan officers a new level of responsibility. They must effectively explain terms and concepts, like credit history and down payment assistance, to buyers who may be new to hearing them.

“As a result of where Gen Z’ers are in the process — super early — working with a lender that excels in financial literacy has never been more important,” Sher notes.

Indeed, most Gen Z’ers aren’t quite ready to buy their first homes, but with its influencer strategy and intake form, NFM Lending is prepared to support them when they are. In the meantime, our data provides unique insights to inform the greater mortgage industry on the best ways to do so.

LINTHICUM, MD, November 7, 2023 — NFM Lending, a leading mortgage company, is excited to announce a significant rebranding effort for one of its core divisions. The company’s Influencer Division will now be known as The Creator Collective, reflecting a strategic shift to more accurately represent the innovative work being done by this dynamic group of social media pioneers.

The name change from Influencer Division to The Creator Collective is more than just a semantic shift; it’s a reflection of the division’s evolution and the multifaceted nature of their contributions. In the digital age, these individuals do far more than merely “influence” others. They are content creators and educators who hold the key to financial empowerment. They particularly play a vital role in helping Gen Z homebuyers, who prefer to receive information through videos on apps like YouTube and TikTok, navigate the complexities of the mortgage process.

This rebranding acknowledges the dedication and creativity of each member of The Creator Collective. These individuals invest significant time and effort in crafting valuable, informative, and engaging content related to the mortgage industry. They are true creatives, with distinctive styles and unique niches that set them apart not only from each other but also from online creators in other sectors.

The Creator Collective is committed to producing content that empowers and educates potential homebuyers. They craft insightful narratives, offer expert advice, and use their creativity to demystify the home-buying process. As a result, they are increasing financial literacy, making it more accessible to a broader audience, especially Gen Z buyers, a burgeoning set of prospective homebuyers.

This rebranding effort underscores the true essence of the division’s mission. The name The Creator Collective better signifies the work they are doing and the significant value they bring to online content in the mortgage industry. By embracing this new name, NFM Lending is reaffirming its commitment to innovation in social media and excellence in mortgage lending.

NFM Lending is excited to embark on this new chapter with The Creator Collective and looks forward to the continued impact and inspiration they will bring to the world of homeownership and mortgage education.

For more information about NFM Lending and The Creator Collective, please email TheCreatorCollective@nfmlending.com.

About NFM Lending

NFM Lending is a national mortgage lending company currently licensed in 49 states and Washington, D.C. The company was founded in Baltimore, Maryland in 1998. NFM Lending and its family of companies include Main Street Home Loans, BluPrint Home Loans, Elevate Home Loans, and Element Home Loans. They attribute their success in the mortgage industry to their steadfast commitment to customers and the community. For more information about NFM Lending, visit www.nfmlending.com, like our Facebook page, or follow us on Instagram.