Are you looking to update your bathroom but need to do so on a budget? Use this list of bathroom renovation ideas to inspire your next DIY project.

The quickest way to give your bathroom a refresh is by simply giving it a new coat of paint. However, don’t be mistaken into thinking it will be an easy DIY project. Your bathroom is full of nooks and crannies that you’ll have to paint around (such as toilets and showers). When choosing colors, stick with earth tones for a spa-like feel. If you want to give it modern twist, choose an accent wall to make a bright color that really pops.

Just because it’s a bathroom doesn’t mean you can’t feature some cool wall decor. Hang up some paintings or mirrors. If you have the space, add a couple shelves for plants, frames or even signs. The possibilities are endless.

Swap your same old boring rectangle or square mirror for a fun shape! It can be a circle, or even a collage made up of a couple mirrors. You’d be surprised at how much different a room can feel by making just this one change.

Give the hardware in your bathroom an update. Replace your faucet, knobs, light fixtures and towel racks. Give your shower head an upgrade. If it’s in your budget, consider replacing your sink entirely.

Don’t let your tight budget hold you back. Rather than replacing the entire vanity, repaint or stain it. This will make it feel like new without draining your wallet. If you do want to replace it, don’t buy new – upcycle! A vintage table or dresser might require some work but will be well worth it!

Giving your bathroom a makeover doesn’t need to be costly. There are plenty of bathroom renovations you can do yourself. If you are looking for a larger-scale remodel, there are several financing options available.

If you have any questions or want more information about what options are available to you, contact one of our licensed Mortgage Loan Originators.

As the weather starts to warm up, homeowners might begin thinking about home improvement projects. That’s why May is National Home Remodeling month! Owning a home is one of the biggest investments you’ll make, so it’s important to keep up with home maintenance.

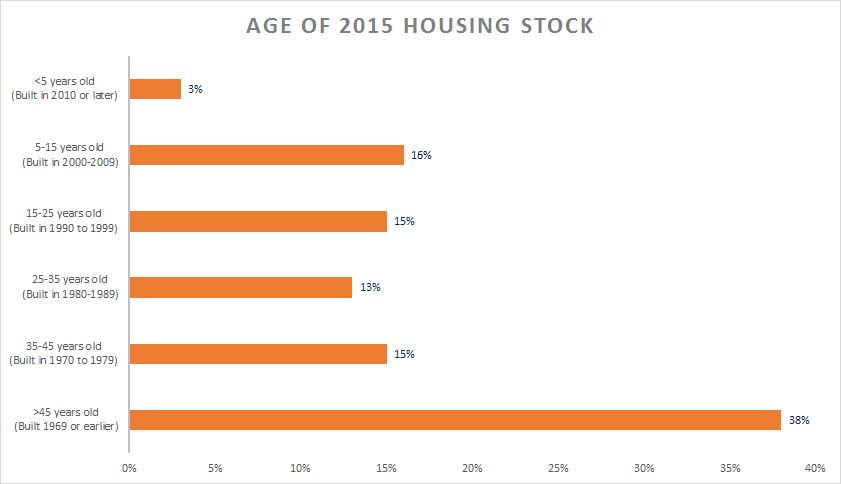

As of 2015, 66% of the US owner-occupied housing stock was built before 1980, with around 38% built before 1970, according to the National Association of Home Builders (NAHB). Many of these homes are going to need repairs, renovations, or updates.

There are many renovation and repair loan options available, but we will focus on three: Conventional, FHA, and VA renovation. If you are looking for financial assistance for projects or you’re considering purchasing a home that needs a little TLC, here are a few loan programs for home remodeling.

The FHA 203(K) renovation loan allows a qualified borrower to purchase or refinance a home and finance the cost of renovations/repairs into the overall final loan. (Not to exceed 110% of the after-improved value of the home). The repairs allowed on a 203(K) are not restricted to FHA required repairs that would be deemed necessary by a consultant and/or appraiser but can include a “wish list” of items such as:

Luxury items such as installation of a pool, BBQ pit, or even a hot tub are not allowed.

FHA offers two versions of the 203k program, Limited 203(K) and Standard/Full 203(K). All work must be completed within 180 days of closing.

This program allows the borrower to finance into the loan limited/non- comprehensive repairs:

NFM Lending requires a minimum of $3,500 in repairs for this program. A HUD consultant is not required to perform an inspection of the property on this type of renovation program but may be used.

Work cannot displace the borrower from the home for more than 15 days. If the house will be vacant for longer than 15 days, the Standard 203(k) must be used. The Limited program allows a disbursement at closing up to 50% of the estimated materials and labor costs before beginning construction but only when the contractor is not willing or able to defer receipt of payment until completion of the work, or the payment represents the cost of materials incurred prior to construction.

The Standard/Full 203(K) program allows the borrower to finance in many more items than the limited program. Repairs with this type of 203(K) can include structural alterations, conversions from 1 to 4 units, work that requires plans, and many more. A HUD-approved consultant is required. The borrower must meet with the consultant to determine not only the mandatory items but any “wish list” items that are to be included in the cost of repairs.

With the Standard program, the borrower can be displaced from the home for up to 6 months. Mortgage payments can be financed into the loan for the time that the house is deemed uninhabitable during the renovation period. The HUD consultant will deem the number months that can be financed into the loan. Please inquire as to the availability of financing in mortgage payments with your 203K specialist.

The Fannie Mae HomeStyle® Renovation loan allows a qualified borrower to purchase or refinance a home and finance the cost of renovations/repairs into one final loan. (The total renovation cost cannot exceed 75% of the after completed value of the home based on the appraisal or the total acquisition cost, whichever is less). The sales price plus the total cost of renovations is considered the total acquisition cost. All repairs must be completed within 180 days of closing.

This program allows the borrower to finance into the loan limited/non-comprehensive repairs:

NFM Lending requires a minimum of $3,500 in repairs for this program. A HUD consultant is not required to perform an inspection of the property on this type of renovation program but may be used.

The Standard/Full HomeStyle® program allows the borrower to finance any type of repair including structural alterations and repairs, additions, work that requires architectural plans, and much more. The borrower must meet with a HUD consultant to determine the repairs to be included into the loan.

Up to 6 months mortgage payments can be financed into the loan for the time that the HUD consultant deems the house uninhabitable during the renovation period. Please inquire about the availability of mortgage payment financing with your renovation specialist.

The VA renovation loan is a great option for Veterans who may be buying a home that needs a little work, or perhaps they want to do some modernization to their current home.

This program allows the borrower to finance into the loan limited/non-comprehensive repairs:

Click here for more information about how to finance renovations or home improvements.

Every home is unique and will require varying repairs and updates. But with these mortgage loan options, your dream of updating your home or becoming a homeowner are possible!

You can also keep in mind the possibility of building your home from the ground up as there are many construction loan options available as well.

If you have any questions about renovation loans or want more information about the homebuying process, contact one of our licensed Mortgage Loan Originators. If you are ready to begin the process, click here to get started!

*Total renovations must not exceed $35,000; this is inclusive of repair amount, contingency of 10-15%, inspection fees, title update, permits and renovation fee.

So, you’ve decided you want to buy a fixer-upper. Homes that require a little bit of TLC are a great choice as there is typically less competition in the housing market. However, they aren’t for the faint of heart. These homes require more time spent planning and usually a bit more work. If you’re up for the challenge, you will most likely discover plenty of benefits. Let us get you on the road to homeownership by answering your first question: what is an FHA 203(K) rehab loan?

The FHA 203(K) rehab loan (also known as a renovation loan) allows a qualified borrower to purchase or refinance a home and finance renovations with a single loan. The convenience of this single loan removes the frustration and stress of having to apply for multiple loans.

The cost of renovations/repairs are not to exceed 110% of the after-improved value of the home.

The repairs allowed on a 203(K) are not restricted to FHA required repairs that would be deemed necessary by a consultant and/or appraiser, but can include a “wish list” of items such as:

Luxury items such as installation of a pool or fire pit are not allowed.

FHA offers two versions of the 203(K) program.

Limited 203(K)

This program allows you to finance into the loan limited/non- comprehensive repairs:

NFM Lending requires a minimum of $3,500 in repairs for this program. A HUD consultant is not required to perform an inspection of the property on this type of renovation program but may be used.

Work cannot displace you from the home for more than 15 days. If the house will be vacant for longer than 15 days, a Standard 203(k) must be used. The Limited program allows a disbursement at closing, up to 50% of the estimated materials and labor costs before beginning construction, but only when the contractor is not willing or able to defer receipt of payment until completion of the work, or the payment represents the cost of materials incurred prior to construction.

Standard/Full 203(K)

The Standard/Full 203(K) program allows you to finance in many more items than the limited program. Repairs with this type of 203(K) can include structural alterations, conversions from 1 to 4 units, work that requires plans, and many more. A HUD approved consultant is required. You must meet with the consultant to determine not only the mandatory items but any “wish list” items that are to be included in the cost of repairs.

With the Standard program, you can be displaced from the home for up to 6 months. Mortgage payments can be financed into the loan for the time that the house is deemed uninhabitable during the renovation period. The HUD consultant will deem the number months that can be financed into the loan. Please inquire as to the availability of financing in mortgage payments with your 203(K) specialist.

All loans require the use of a licensed contractor. Any repairs including the cost, materials used, scope of work, etc., should be completely decided upon prior to closing. You cannot act as your own contractor, and you cannot be related to the contractor. The contractor must be licensed and insured as a home improvement contractor and/or specialty contractor in the state or local jurisdiction where the work is being done. Choosing the right contractor is crucial to making sure that there are no issues after the work begins. It’s very important to obtain the contractors credentials up front and present them to NFM Lending for review as soon as possible.

While choosing to purchase a home that needs renovations isn’t as easy, it does provide several benefits. You’ll face less competition while purchasing and you’ll have higher equity then you would when buying a move-in ready home. If you’re ready to achieve your dreams of homeownership, include an FHA 203(K) rehab loan when considering your options.

For more information about the FHA 203(K) loan or other renovation loans, contact one of our licensed renovation loan originators. If you are ready to buy a home, click here to get started!

If you’re looking to buy a home, be prepared to meet a few challenges with today’s housing market. Not only is there a shortage of homes, but the available housing stock is aging. These challenges might seem discouraging but taking a look at the 2018 housing market and what options you have as a homebuyer, it is still possible to find a home to make your own.

As of 2015, 66% of the US owner-occupied housing stock was built before 1980, with around 38% built before 1970, according to the National Association of Home Builders (NAHB). Many of these homes are going to need repairs, renovations, or updates.

And while there are a lot of new homes being built throughout the country, buyers should not turn away from an older home that may need some TLC. There are many renovation and repair loan options available, such as the FHA 203(K) or Fannie Mae’s HomeStyle® loan. FHA 203(k) are a type of federally insured mortgage loans that are used to fund renovations and repairs of single family properties. Fannie Mae’s HomeStyle® Renovationloan permits borrowers to include financing to renovate or make home repairs a purchase or refinance transaction. Find more information about how to finance renovations or home improvements.

Every home is unique and will require varying repairs and updates. But with these mortgage loan options, your dream of renovating an older home and becoming a homeowner are possible!

You can also keep in mind the possibility of building your home from the ground up as there are many construction loans options available as well.

If you have any questions about renovation loans or want more information about the homebuying process, contact one of our licensed Mortgage Loan Originators. If you are ready to begin the process, click here to get started!

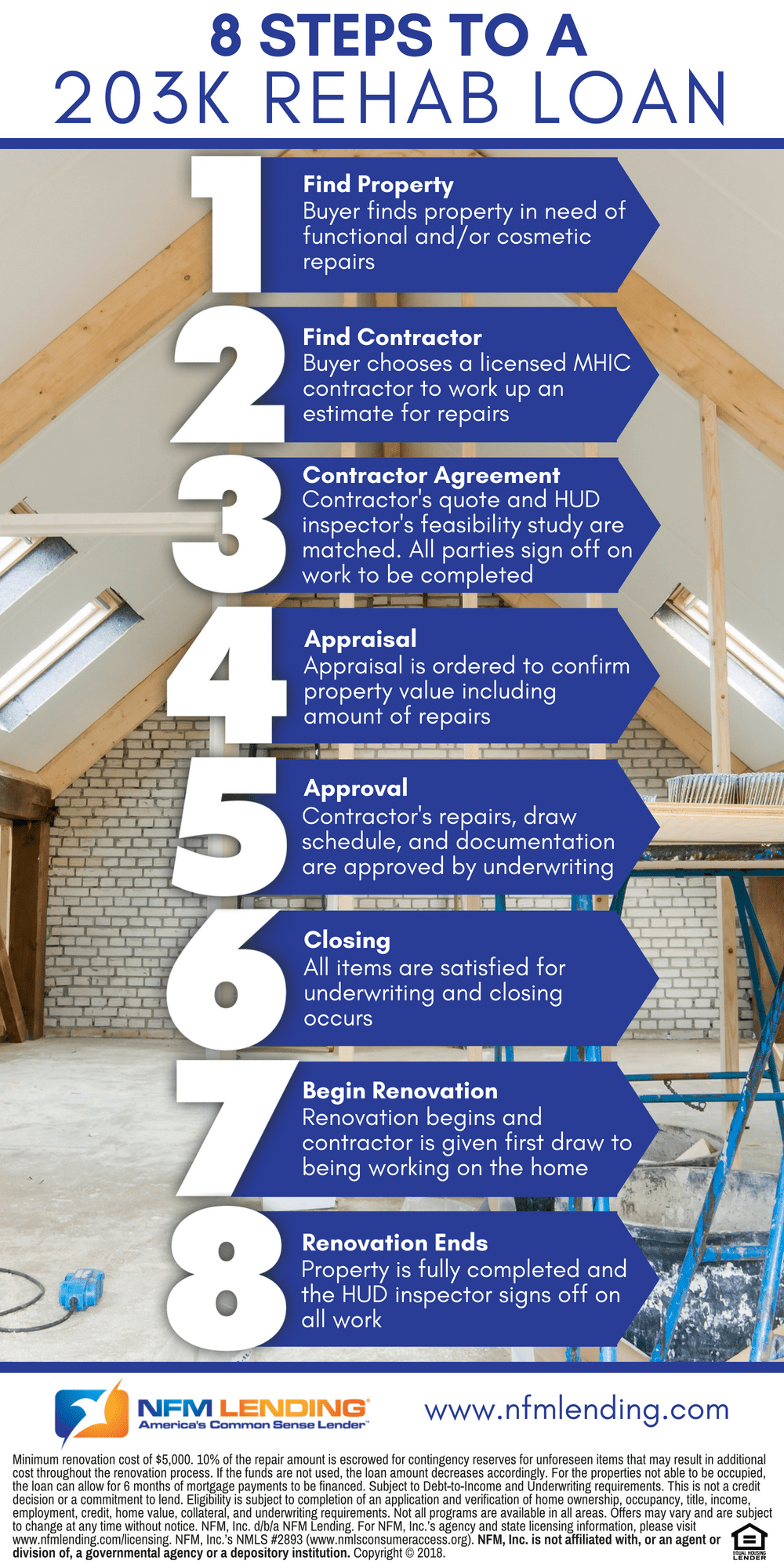

When house-hunting for your new home, you might discover one that would be perfect for you but needs a bit of TLC. Don’t worry! An FHA 203k rehab loan is there to make your dreams of homeownership come true. This loan allows you to borrow both what you need to purchase the home and what you need to make repairs—an all in one mortgage. If you think this might be the option for you, take a look at our 8 steps to a 203k rehab loan.

Don’t be under the impression that you have to buy a house that’s in perfect condition. Renovating and making repairs will allow you to create exactly what you want, so keep this option in mind when you’re ready to find the home of your dreams!

You can find out more about 203(k) rehab loans here. For questions or more information about the homebuying process, contact one of our licensed Mortgage Loan Originators. If you are ready to begin the process, click here to get started!