Time's up

Are you looking to buy a home but are stumped with some of the terms that Real Estate Agents, Loan Originators, or even websites say? Here are the most commonly used mortgage terms and definitions to help you through the home buying and loan process:

Adjustable-Rate Mortgage (ARM) – An ARM, also known as a Variable Rate Mortgage, is a loan with an interest rate that is periodically adjusted based on a pre-determined index.

Annual Percentage Rate (APR) – The APR is the cost of a mortgage stated as a yearly percentage rate. Since the APR includes points and other credit costs, it is typically higher than the advertised note rate. An APR allows home buyers to compare different mortgages based on loans’ annual costs.

Appraisal – An appraisal is a written analysis, prepared by a qualified appraiser, of a property’s estimated value.

Buy-down – A buy-down is when a lender or builder subsidizes a loan by lowering the interest rate during the initial years of a loan. Payments increase when the subsidy expires.

Closing Costs – The fees charged for services performed, including the home appraisal, loan origination, flood certificate, the title survey, etc.

Debt-to-Income Ratio – This is the ratio that results when a buyer’s monthly payment obligation on long-term debts is divided by his or her gross monthly income.

Down Payment – The part of a property’s purchase price paid by the borrower (i.e., not financed by the mortgage). Down payments can be anywhere from 3-20 percent of the purchase price.

Earnest Money – Earnest money is paid by the buyer to the seller to bind a transaction or assure payment.

Escrow – Escrow is the holding of funds or documents by a third party prior to closing; the funds are usually for payment of taxes and insurance on property.

Fixed-Rate Mortgage – A fixed-rate mortgage has interest rates that remain constant during the repayment period.

Home Equity – Equity is created when the value of your home increases and/or you reduce the amount you owe through your loan payments.

HUD-1 Settlement Statement – Standard, government regulated settlement statement that itemizes the costs of transaction when purchasing a home. Commonly referred to as “HUDs” or “HUD-1s.”

Interest Rate – Also known as the “note rate”, the interest rate is the cost the borrower agrees to pay the lender for borrowing money to finance a loan. The interest rate is shown as an annual percentage of the outstanding loan amount (principal).

Lock-in – A lock-in is a written agreement guaranteeing a borrower a specific interest rate as long as the loan closes and funds before a certain date. A lock-in usually specifies the number of points paid at closing.

Negative Amortization – On negative amortization loans, your monthly payments may not cover all of the interest due. When that happens, the unpaid interest is added to your mortgage balance so that you would owe more on your mortgage than you originally borrowed.

Origination Fee – Fee(s) charged by the lender to the borrower to prepare loan documents, conduct credit checks, inspect and sometimes appraise property. Origination fees are usually charged as a percentage of the loan.

PITI – A borrower’s monthly mortgage payment: Principle, Interest, Taxes, and Insurance.

Points – Fee assessed by the lender, usually to permanently buy a below-market rate. One point equals 1 percent of the loan amount. For example, three points on a $100,000 mortgage is $3,000.

Pre-Paids – Expenses such as interest and escrow reserves.

Prepayment Penalties – Fees that the borrower will incur if the mortgage is fully paid during a “prepayment penalty period”.

Private Mortgage Insurance (PMI) – PMI, which protects lenders against loss if a borrower defaults, is typically required for borrowers making a down payment less than 20 percent. PMI typically requires an initial premium payment of 1-5 percent and also has a monthly fee.

Real Estate Settlement Procedures Act (RESPA) – RESPA is a federal law that allows consumers to review information on known or estimated settlement costs once after application and once prior to or at a settlement. The law requires lenders to furnish the information after application only.

Settlement/Closing – Closing is the meeting between buyer, seller, and closing officer (a lawyer or title/escrow company representative depending on the state) where the property and funds legally change hands by signing all relevant documents.

Settlement Costs – Combination of hard closing costs and pre-paids. Settlement Costs include the origination fee, discount points, appraisal fee, title search and insurance, survey, taxes, deed recording fee, and all other costs.

Underwriting – Underwriting is the process during which the decision is made whether to approve a loans rates and terms based on the borrowers’ credit, employment, assets, and other factors.

Yield Spread Premium (YSP) – A rebate by a lender or investor to a local Loan Officer for closing a loan on a certain product.

Should you have any questions about these mortgage terms or any other that you may have encountered, please contact us!

Do you know what the difference is between Interest Rate and APR? These two items are key terms to know when researching mortgage loans. Here are their definitions:

Interest rate is the rate at which interest is paid by borrowers for the use of money that they borrow from a lender. This is important to note when comparing quotes for different loans since it directly affects your monthly payments.

Annual Percentage Rate (APR) describes the interest rate for a whole year (annualized), rather than just a monthly fee/rate, or more simply, it is a finance charge expressed as an annual rate. The APR is a broader measure of cost to you of borrowing money, and reflects not only the interest rate but also the points, broker fees, and other charges that you have to pay to get the loan, including some of your closing costs. For that reason, your APR is usually higher than your interest rate. The APR can help consumers understand the differences between the interest rate and the fees paid at closing. This was established as a part of the Truth in Lending Act.

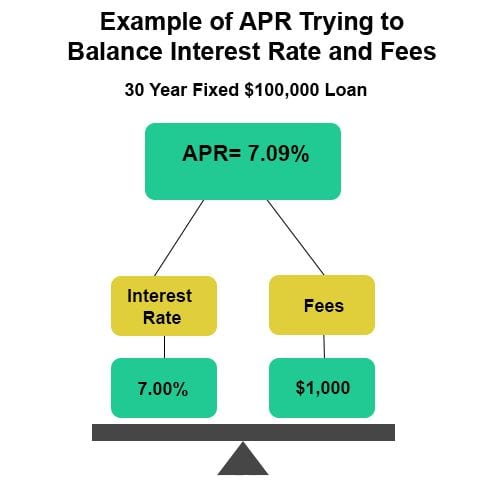

Below is a diagram that shows how APR tries to balance (and incorporate) both interest rates and fees.

How APR is Determined

To calculate the APR, the fees required to finance the loan are added to the interest rate. These are able to be combined by amortizing (paying off debt in regular installments over a period of time) the fees over the course of the loan, and calculating a new rate.

If you have any questions about interest rate and APR during your loan process, click here to talk to one of our Licensed Mortgage Loan Originators today!