LINTHICUM, MD, October 5, 2015 — NFM Lending is pleased to announce the opening of a new branch in New Orleans, Louisiana. The branch will focus its lending platform throughout the New Orleans area. NFM Lending offers Conventional, FHA, VA, USDA, FNMA, Jumbo, and many other loan options. Visit the branch page to learn more: https://nfmlending.com/la317.

Jennifer Cook, Branch Manager, has worked in the mortgage industry for over 10 years. She has been part of the NFM Lending family since 2009 as a Loan Originator and Branch Manager, working out of the Corporate office in Linthicum, Maryland. She looks forward to the opportunity expand her business to the great state of Louisiana.

“I have been with NFM lending since 2009 and decided to branch out into a new location,” said Cook. “I have stayed with NFM because of their commitment to getting loans closed with the least stress possible for my buyers. NFM has great people in both the front and back of the house that truly care about our clients. Our strong operations team means I can focus on growing my business and helping people get into their dream homes.”

The New Orleans branch currently has openings for qualified Mortgage Loan Originators for full and part-time positions. The branch’s goal is to continue to provide the same commitment and dedication to borrowers ranging from first time homebuyers, to seasoned buyers looking for their next home, a second home, or investment properties.

NFM Lending is a mortgage lending company currently licensed in 29 states across the U.S. The company was founded in Baltimore, Maryland in 1998. They attribute their success in the mortgage industry to their steadfast commitment to customers and the community. NFM Lending has firmly planted itself in the home loan marketplace as “America’s Common Sense Residential Mortgage Lender.”

The TILA-RESPA Integrated Disclosure (TRID) Rule will take effect on October 3, 2015. TRID will significantly change the way real estate transactions are processed and settled. To avoid delays and to ensure that each settlement goes as smoothly as possible, it is important for real estate agents to be informed of all of the changes TRID will introduce to the closing process.

New Documents When TRID goes into effect, there will be two new disclosure forms: the Loan Estimate (LE) and the Closing Disclosure (CD). The LE will combine and replace the Good Faith Estimate and the Truth in Lending disclosure. The CD will combine and replace the HUD-1 and the final Truth in Lending disclosure.

The LE is a form that explains the loan’s features, terms, and risks. This form is due to the borrower within three days of their submitting a loan application. The CD provides the borrower with final details about the loan, including projected monthly payments, fees, and other costs. This is due to the borrower at least three days before closing.

New Timeline The new disclosures will also instate new timelines for real estate transactions. The lender now has two new deadlines. They are required to provide the borrower with the LE at least three business days after loan application, and to provide the borrower with the CD at least three business days before loan consummation. Click here to view a timeline chart.

The latter deadline can, in some instances, delay closing. If the lender does not provide the borrower with the CD three days before closing, a scheduled closing may be delayed. Additionally, there are some cases in which a re-disclosure, or another three-day review period, will be necessary. If the lender provides the borrower with the CD, and the loan terms in the CD are significantly different from those detailed in the LE, a re-disclosure will be required. Richard Cordray, Director of the Consumer Financial Protection Bureau (CFPB) has specified the following three situations under which re-disclosure would be necessary:

An APR increase of more than 1/8 of a percent for fixed-rate loans, or 1/4 of a percent for adjustable loans (A decrease in APR will not require re-disclosure if it is based on changes to the interest rate or other fees.)

The addition of a prepayment penalty

The loan product itself changes, (i.e., from fixed-rate to adjustable-rate)

Preparing Clients for these Changes

In order to avoid closing delays or confusion when TRID goes into effect, it is important to spend some time reviewing the new forms, so that you can answer any questions your client may have. Keep the new timelines in mind when drawing up contracts, coordinate closings carefully, and avoid any last-minute changes or negotiations. Encourage your clients to review the documents they receive carefully, and to communicate with the lender and ask questions. Finally, avoid making promises that cannot be kept. Initially when the new disclosure forms are implemented, loans and purchases may take longer to close. Make sure your clients are prepared for this possibility.

Knowing how Know Before You Owe, or TRID will change the mortgage industry will help you better serve your clients, and prevent delays in closing or other issues. The CFPB and the Mortgage Bankers Association have published resources for real estate professionals to educate themselves and their clients on TRID. These resources can provide further information and answer some of your questions about how these changes will affect you and your clients.

For more information about TRID, and how NFM Lending is preparing for TRID, click here.

The Consumer Financial Protection Bureau (CFPB) has released new online tools on their “Owning a Home” landing page. These tools are aimed at helping consumers better understand the mortgage process, in preparation for the TILA-RESPA Integrated Closing Disclosures (TRID), or the Know Before You Owe Rule, which goes into effect October 3, 2015.

The new tools are divided into four phases:

Prepare to shop

Explore loan choices

Compare loan offers

Get ready to close

Within each phase, consumers can use various online forms and worksheets to learn more about the loan process and their options. Consumers can, for example, explore potential interest rates, based on their credit score, location, home price, loan type, and more. There are also tools that walk consumers step-by-step through the new disclosure forms: the Loan Estimate and the Closing Disclosure.

NFM Lending is continuing to prepare its employees, industry partners and consumers for TRID. For more information on TRID, and to find out what NFM Lending is doing to prepare, click here.

LINTHICUM, MD, August 28, 2015— NFM Lending is proud to announce David Silverman, CEO, has been named one of the 100 Most Influential Mortgage Executives in America by Mortgage Executive Magazine for 2015.

Each year, Mortgage Executive Magazine recognizes mortgage executives that have built their companies and service their clients and employees through service, dedication and hard work. The winning executives were asked to provide their insights on the mortgage industry’s opportunities and challenges today. Silverman spoke about NFM Lending’s increased focus on selective recruiting:

“The biggest opportunity for NFM Lending this year is to be selective with our origination recruits and focus on better, not bigger. Fortunately, the demand for service and product remains very high with a smaller supply of human capital across the industry. We believe this is a great time to be selective as well as bring new blood into the mortgage space and train them up.”

This is the third year in a row that Silverman has received this award.

“I am truly honored to be recognized again amongst so many spectacular leaders in our industry,” said Silverman. “All I can do is continue to work towards being the best leader I can be for my company and those that I am blessed to have on my team making me look good. I surround myself with the best, and occasionally some of it rubs off on me.”

NFM Lending has prospered under Silverman’s leadership, and continues to receive national recognition. The company was named one of the 50 Best Companies to Work For in 2015 by Mortgage Executive Magazine; one of the Washington Post’s Top Work Places in the Washington, D.C. area in 2015; a Top Mortgage Employer by National Mortgage Professional Magazine in 2015; and a Top Work Place in the Baltimore area by The Baltimore Sun in 2012, 2013, and 2014.

NFM Lending was founded in March of 1998 by David Silverman and his wife Sandy. The company started as a small brokerage shop with 4 loan originators and is now a multi-state lender with more than 350 employees, 39 retail branches, and is licensed in 29 states.

NFM Lending is a mortgage lending company currently licensed in 29 states in the U.S. The company was founded in Baltimore, Maryland in 1998. They attribute their success in the mortgage industry to their steadfast commitment to customers and the community. NFM Lending has firmly planted itself in the home loan marketplace as “America’s Common Sense Residential Mortgage Lender.”

For information on NFM Lending, please email pr@nfmlending.com.

The new Loan Estimate and Closing Disclosure documents will replace the Good Faith Estimate, the HUD-1, and the Truth in Lending Statement on most residential loan transactions. This change is anticipated to have wide-reaching effects on the mortgage and real estate industries.

The TRID changes were originally scheduled to take place August 1, 2015; however, after pressure from Congress and industry groups to delay this deadline, or to provide a grace period, the CFPB issued a proposal to move this date to October 3, 2015. The proposal was open for public comment on the CFPB website until July 7, 2015. In their press release announcing the delay, the CFPB stated that it believes scheduling the effective date on a weekend will “facilitate implementation by giving industry time over the weekend to launch new systems configurations and to test systems.”

NFM Lending is continuing to prepare its employees and clients for TRID. For more information about this new rule, and what NFM Lending is doing to prepare, click here.

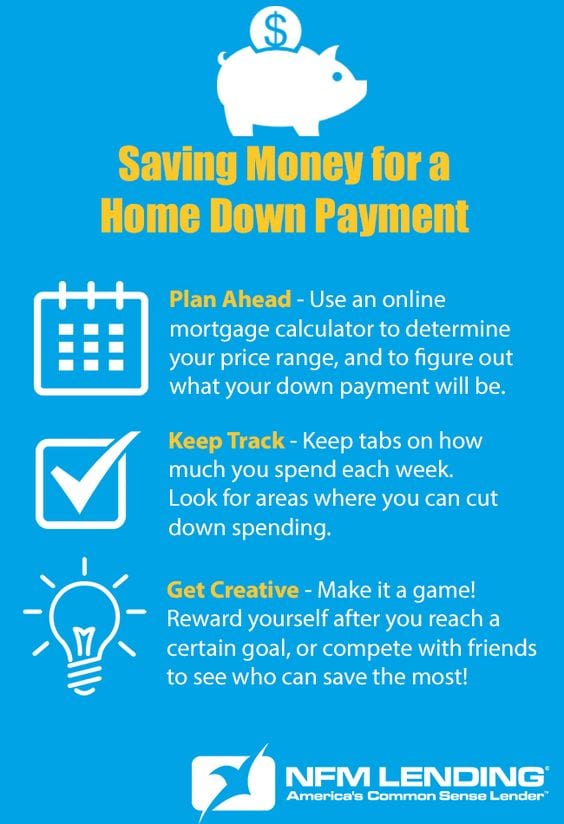

Like any major purchase, a home purchase will require you to put down a certain percentage of the total price as a down payment. The bigger the down payment, the less you will borrow from the mortgage company or bank, and the less your payments will be. With every day expenses and current bills, it can be difficult to find money to begin saving for a down payment. By planning ahead and getting creative, you can begin to save up for a down payment for the mortgage loan that best suits your needs. Here are three ways to save for a down payment and help come up with the savings you need to land the house of your dreams.

Planning Ahead

Saving money for a down payment may take a while, so it helps to have a plan. Start by researching what kind of home you are looking to buy, and the average price of those homes in the area. Then, use an online mortgage calculator to find out what kind of down payment options are best for you, based on your price range. For example, if the homes in the neighborhood you are looking to buy average at $200,000, the standard 20% down payment will be $40,000. Remember, there are loans available with lower down payment options, such as 10% and as low as 3.5%. Talk to your Loan Originator to find out which loan option is right for you.

Once you determine your down payment goals, open a separate savings account. If you’re a first-time home buyer, you can open an investment retirement account (IRA). An IRA will accumulate interest, and first-time home buyers can withdraw up to $10,000.00 from their IRA without a penalty fee. Consult a CPA for more information. Having a separate account for your down payment savings prevents you from accidentally confusing the money with your regular spending money, and it is a good way to track your progress.

Saving money will be easier if you have goals in mind. Set realistic weekly, biweekly, or monthly savings goals, and stick to them. If your workplace offers this option, set up your direct deposit so that a portion of each paycheck automatically goes into the savings account you have set aside for your down payment.

Hold Yourself Accountable Saving money will probably require a lifestyle change, and some habits are difficult to break. For instance, if you are used to going out to eat for lunch five days a week, it will be hard to start trying to pack a lunch every day. Set up a time a few times a month, or even once a week, to sit down and go over your expenditures from the week(s) before. Seeing when and how often you make unnecessary purchases can motivate you to make the changes you need to make. Have a close friend or significant other help hold you accountable, (if you’re buying a home together, you can do this for one another).

Providing incentives for yourself can also be a helpful tactic. Set monthly savings goals, and reward yourself at the end of the month if you meet your goals. If your goal is to save $500.00 in a month, and you reach that goal, reward yourself with a small splurge—go out to dinner with friends, or buy yourself something new. This will encourage you to meet your savings goals, and the splurge will be guilt-free, because you have already met your goal for the month.

Get Creative Although the process of saving for a down payment may seem daunting, it doesn’t have to be a chore. There are lots of fun, creative ways to save money. One idea is to earn extra money on the side. Offer to do some odd jobs, such as babysitting, dog walking, home repairs, or housework for your friends or neighbors. If you’re crafty, open an Etsy store and sell your items online. You might be surprised by how much your woodworking, knitting, graphic design, or other skills are in demand. You can also sell clothes or household goods that you’re not using anymore on sites like Craigslis and eBay, or at your local consignment store.

Another way to get creative about saving is to turn it into a game. Have a competition with a friend or family member who is also trying to save money, and see who can save the most by a particular deadline. If you’re buying a home with your significant other, compete with one another, and see how much you can save together!

The decision to buy a home is one of the biggest financial decisions you will ever make. It is important to plan and prepare carefully. Saving money for a down payment can be difficult, but it is well worth the challenge. If you’re thinking about buying a home soon, get started by talking to one of our licensed Mortgage Loan Originators today.

Stobbe was invited to speak at the expo as a recognized expert in the mortgage industry. She will deliver two seminars at the expo, the first titled “3 Massive Mortgage Money Mistakes to Avoid” and “Why Shopping for the Best Interest Rate can cost you Money”; the second titled “7 Massive Mortgage Mistakes to Avoid” and “VA, FHA & Conventional Financing Highlights.”

“I am thrilled to be a part of the FL Times Union Home Buyer’s Expo!” said Stobbe. “An educated consumer is our best client. I consider it a professional responsibility and I am passionate about empowering home buyers to understand the details about how their mortgage affects their home buying options. I am proud to help raise the standard in mortgage lending by giving home buyers the tools and questions to ask when shopping for a mortgage. I hope that my new book, How to Get Approved for the Best Mortgage Without Sticking a Fork in Your Eye, helps home buyers make smarter decisions with their loan options.”

The Home Buyers Expo will take place from 9:00 a.m. to 3:30 p.m. at the University of North Florida (UNF) University Center. The event is expected to draw attendance from more than 1,500 prospective home buyers and sellers. It will feature speakers on various industry topics, as well as informational booths hosted by real estate agents, builders, mortgage companies, home improvement vendors, and more.

For more information about sponsorship or attendance, call (904)-359-4024. To contact Elysia Stobbe, call her at (904) 446-9007 or visit her website: www.nfmlending.com/estobbe.

About NFM Lending

NFM Lending is a mortgage lending company currently licensed in 29 states across the United States. The company was founded in Baltimore, Maryland in 1998. They attribute their success in the mortgage industry to their steadfast commitment to their customers and their community. NFM Lending has firmly planted itself in the home loan marketplace as “America’s Common Sense Residential Mortgage Lender.”

For more information about NFM Lending, please contact:

LINTHICUM, MD, June 26, 2015 — Elysia Stobbe, a NFM Lending Branch Manager in Jacksonville, FL, released her book, How to Get Approved for the Best Mortgage Without Sticking a Fork in Your Eye, on June 26, 2015.

The book walks potential home buyers through the steps of applying for a home loan: from types of loans, to choosing a mortgage professional, the application process, fees and paperwork, mortgage insurance, and more. Stobbe believes there is a plethora of confusion and misunderstanding among first time homebuyers about loan programs and choosing a mortgage lender. She wrote this book using her expertise to help home buyers understand their options, and navigate the mortgage process successfully.

“My commitment to client service has driven my passion for the individual personal experience in the mortgage industry, and how the regulations and requirements affect real people in real time,” said Stobbe. “With this book I’m privileged and excited to share my knowledge and experience. After reading this book, you will have an understanding of the requirements of the lenders that loan money to home buyers, what loan options you have, and how to navigate government regulations and requirements to your advantage.”

Stobbe has over 12 years of experience in the mortgage industry, and has closed over $250 million in residential mortgage loans. She has been interviewed by the Wall Street Journal and the Washington Post about her mortgage lending expertise. Stobbe has also been ranked a Top Lender in Northeast Florida by Jacksonville Business Journal three years in a row, and recognized as a 2014 Top 50 Business Influencer by Advantage Magazine.

To purchase How to Get Approved for the Best Mortgage Without Sticking a Fork in Your Eye, click here. To contact Stobbe directly, visit her website at www.nfmlending.com/estobbe, contact her at 904-446-9007 or email her at estobbe@nfmlending.com.

About NFM Lending

NFM Lending is a mortgage lending company currently licensed in 29 states in the U.S. The company was founded in Baltimore, Maryland in 1998. They attribute their success in the mortgage industry to their steadfast commitment to customers and the community. NFM Lending has firmly planted itself in the home loan marketplace as “America’s Common Sense Residential Mortgage Lender.™” For more information about NFM Lending, visit www.nfmlending.com, like our Facebook page, or follow us on Twitter.

NFM Lending is currently holding its annual food drive at its corporate and retail branch locations throughout the U.S. From June 1-30, 2015, NFM Lending employees and their friends and family members will bring in canned goods and other non-perishable food items into their local NFM Lending location. Donations collected in Maryland will go to the Maryland Food Bank, while donations collected outside of Maryland will go to local area food banks.

NFM Lending’s food drive is open to the public. If you are interested in participating, please visit our website, http://www.nfmlending.com/find-a-branch to locate a branch near you. The following items were listed on the Maryland Food Bank’s “Most Needed Items” list:

CANNED PROTEIN Tuna

Salmon

Chicken

Peanut Butter

Beans

PASTA & RICE Brown & white rice

Macaroni & cheese

Pasta

FRUITS & VEGETABLES Canned vegetables (low sodium, no salt added)

Fruits & juices (light syrup)

Fruit cocktail

Apple sauce

DAIRY FOODS Shelf-stable milk

Evaporated milk

Infant formula

NON-FOOD ITEMS Diapers

Toilet Paper

Plastic/Paper plates and cups

Sanitary napkins and tampons

Thank you in advance for your support!

LINTHICUM, MD, May 29, 2015 — NFM Lending is pleased to welcome Roger Dennis to the NFM Lending family. Dennis will operate out of NFM Lending’s Corporate Office, located at 505 Progress Drive, Suite 100, in Linthicum, MD.

Dennis has more than 13 years of experience in the lending, real estate, and construction industries in the Washington, D.C. area. He plans to continue to focus on this area, offering Conventional, FHA, VA, USDA, FNMA, Jumbo, and many other loan options. Dennis looks forward to further growth with NFM Lending, while continuing to provide unparalleled customer service and responsiveness.

“I am very excited to be part of the NFM team,” said Dennis. “NFM has an outstanding reputation, both locally and nationwide, for its commitment to the community and its excellence in lending. By working with my team, my clients understand that they are working with one of the best lenders in the industry, and that they have the competitive advantage in the Washington, D.C. metro market.”

Dennis is currently growing his team and is actively recruiting qualified Mortgage Loan Originators, for both full and part-time positions. Their team goal is to continue to provide the highest level of commitment and dedication to every borrower, ranging from first time homebuyers to seasoned buyers looking for second homes or investment properties. Visit his web page to learn more: https://nfmlending.com/rdennis.

NFM Lending (formerly NFM, Inc.) is a mortgage lending company currently licensed in 29 states across the country. The company was founded in Baltimore, Maryland in 1998. NFM attributes its success in the mortgage industry to a steadfast commitment to customers and the community. NFM Lending has firmly planted itself in the home loan marketplace as “America’s Common Sense Residential Mortgage Lender.”

The TILA-RESPA Integrated Disclosure (TRID) Rule will take effect on October 3, 2015. TRID will significantly change the way real estate transactions are processed and settled. To avoid delays and to ensure that each settlement goes as smoothly as possible, it is important for real estate agents to be informed of all of the changes TRID will introduce to the closing process.

The TILA-RESPA Integrated Disclosure (TRID) Rule will take effect on October 3, 2015. TRID will significantly change the way real estate transactions are processed and settled. To avoid delays and to ensure that each settlement goes as smoothly as possible, it is important for real estate agents to be informed of all of the changes TRID will introduce to the closing process. LINTHICUM, MD, August 28, 2015— NFM Lending is proud to announce David Silverman, CEO, has been named one of the 100 Most Influential Mortgage Executives in America by Mortgage Executive Magazine for 2015.

LINTHICUM, MD, August 28, 2015— NFM Lending is proud to announce David Silverman, CEO, has been named one of the 100 Most Influential Mortgage Executives in America by Mortgage Executive Magazine for 2015.

LINTHICUM, MD, June 26, 2015 — Elysia Stobbe, a

LINTHICUM, MD, June 26, 2015 — Elysia Stobbe, a  NFM Lending is currently holding its annual food drive at its corporate and retail branch locations throughout the U.S. From June 1-30, 2015, NFM Lending employees and their friends and family members will bring in canned goods and other non-perishable food items into their local NFM Lending location. Donations collected in Maryland will go to the Maryland Food Bank, while donations collected outside of Maryland will go to local area food banks.

NFM Lending is currently holding its annual food drive at its corporate and retail branch locations throughout the U.S. From June 1-30, 2015, NFM Lending employees and their friends and family members will bring in canned goods and other non-perishable food items into their local NFM Lending location. Donations collected in Maryland will go to the Maryland Food Bank, while donations collected outside of Maryland will go to local area food banks.