One of the biggest reasons holding people back from becoming homeowners is lack of funds, specifically to cover the cost of a down payment on a loan. Luckily, there are several assistance programs available to help people in those financial situations become homeowners by covering the required down payment. If you’re in a tight financial situation, make this the year you become a homeowner by checking out the Chenoa Fund Program.

What is the Chenoa Fund Program?

The Chenoa Fund Program assists borrowers who lack funds by helping them finance the down payment requirement of an FHA loan, which is 3.5%. It essentially combines the ease of an FHA loan with a grant or second mortgage to cover the 3.5% down payment requirement, meaning you receive could receive up to 100% financing.

There are three different options to choose from based on your income. If your income is the same or less than 115% of your area median income, you might be eligible for a different program than if your income exceeds 115%. Let one of our Mortgage Loan Originators help you determine if and for what kind of assistance you may qualify.

Like any loan option, the Chenoa Fund does have a credit requirement. You must have a minimum of 620 FICO score and all additional FHA loan criteria must be met. In some instances, a non-occupant co-borrower is allowed.

As a homebuyer, you should research and discuss with your lender all the possible loan and program options available to you. If you’re thinking an FHA loan might be right for you, talk with your lender about the Chenoa Fund Program. Being unable to fulfill a down payment requirement is no longer a reason to stall your dreams of becoming a homeowner.

Proceeds from the financing can only be used for down payment. Closing costs and prepaid items are the responsibility of the borrower and must be paid by other FHA eligible sources. Please visit http://chenoafund.org/ for more information.

If you are in the market for a new home, one of the first things you should consider financially is how much of a down payment you can make. Most home buyers know that the most common mortgage loan (a Conventional loan) requires 20% down payment. This means that if you purchase a home worth $200,000, you must have $40,000 cash available, on top of the closing costs needed to purchase the home. This may deter many potential home buyers from purchasing because they only have a small amount of money saved. However, Conventional loans are only one of the many loan options available. Here are five of the most widely used mortgage loans and their down payment requirements.

FHA Loan – 3.5% Down Payment*

A Federal Housing Administration (FHA) loan is a mortgage loan that is insured by the government’s Housing and Urban Development (HUD) agency. FHA loans require a 3.5% down payment for purchases and it typically offers very competitive rates compared to rates from a conventional loan. Due to the low down payment, FHA Mortgage Insurance Premiums (MIP) are required in order to protect lenders against losses as a result from defaulted mortgages. There is an up-front premium paid at closing, and a monthly premium that is paid along with the monthly mortgage payment. FHA has several guidelines that all loans must meet, such as loan limits, allowable closing costs, and debt ratios.

VA Loan – 100% Financing**

A VA loan is a mortgage loan guaranteed by the U.S. Department of Veterans Affairs (VA). VA loans help service members, veterans, and eligible surviving spouses purchase a home with a competitive interest rate, limited closing costs, no Private Mortgage Insurance (PMI) requirement, and often without a down payment (as long as the sales price doesn’t exceed the appraised value). This is because VA guarantees a portion of the loan, which allows the lender to provide favorable terms. VA loans have several guidelines that all loans must meet, such as eligibility and loan limits.

USDA Loan – No Money Down†

A USDA loan is a mortgage loan guaranteed by the United States Department of Agriculture (USDA). With a USDA loan, home buyers can purchase a home in eligible rural locations with no down payment, and can finance up to 100% of a home’s appraised value, plus closing costs. For eligible borrowers, USDA loans often come with the lowest interest rates and program insurance premiums of all government-backed loans. USDA loans have several guidelines that all loans must meet, including property eligibility and income eligibility.

80-10-10 Loan – 10% Down Payment

Also known as a Piggyback loan, an 80-10-10 loan is a great option for home buyers who have great credit but lack capital, and wish to avoid paying PMI. The mortgage loan works by having 80% of the property value covered by a first loan, 10% of the property value covered by a second mortgage which carries higher interest rates than the first conventional mortgage, and 10% will be covered by the home buyer’s down payment. Loans that are 80% or less of the home value do not require PMI.

State Bond Programs – Specific Assistance

Several U.S. states offer state bond loan assistance programs. These bond programs aim to help first-time home buyers or buyers with low capital by providing below-market interest rates, down payment assistance, long term affordability, and/or other benefits specific to the programs. These loans have program-specific income and occupancy requirements, and limitations.

There are many more mortgage loan options available not mentioned but these are the most commonly used. If you are looking to purchase a home soon, make sure you speak with a licensed mortgage loan originator. Choosing a down payment option is a big decision and a licensed mortgage loan originator can help you find options that best fit your needs. They can also walk you through the loan process and explain to you all of the eligibility requirements for the loan you choose.

*LTV’s of up to 96.5% for FHA loans. **Veterans Affairs loans require a funding fee, which is based on various loan characteristics. †100% financing, no down payment is required. The loan amount may not exceed 100% of the appraised value, plus the guarantee fee may be included. Loan is limited to the appraised value without the pool, if applicable.

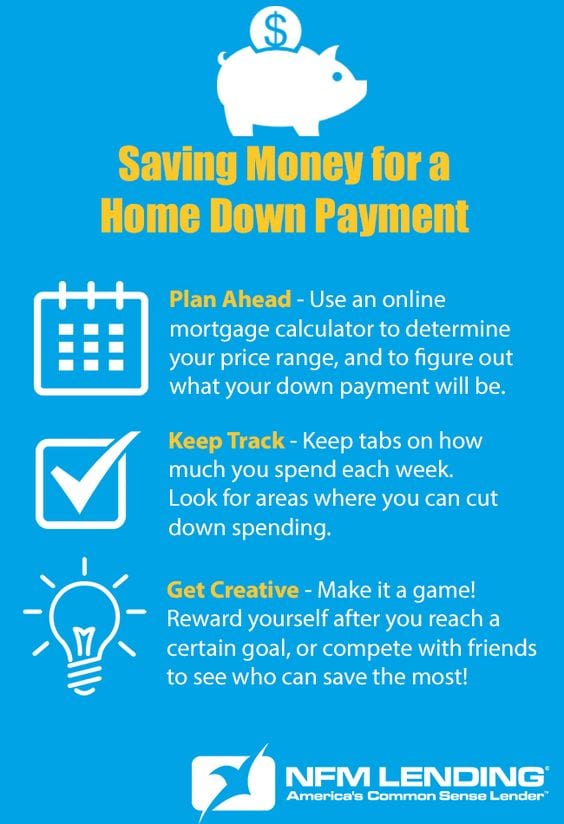

Like any major purchase, a home purchase will require you to put down a certain percentage of the total price as a down payment. The bigger the down payment, the less you will borrow from the mortgage company or bank, and the less your payments will be. With every day expenses and current bills, it can be difficult to find money to begin saving for a down payment. By planning ahead and getting creative, you can begin to save up for a down payment for the mortgage loan that best suits your needs. Here are three ways to save for a down payment and help come up with the savings you need to land the house of your dreams.

Planning Ahead

Saving money for a down payment may take a while, so it helps to have a plan. Start by researching what kind of home you are looking to buy, and the average price of those homes in the area. Then, use an online mortgage calculator to find out what kind of down payment options are best for you, based on your price range. For example, if the homes in the neighborhood you are looking to buy average at $200,000, the standard 20% down payment will be $40,000. Remember, there are loans available with lower down payment options, such as 10% and as low as 3.5%. Talk to your Loan Originator to find out which loan option is right for you.

Once you determine your down payment goals, open a separate savings account. If you’re a first-time home buyer, you can open an investment retirement account (IRA). An IRA will accumulate interest, and first-time home buyers can withdraw up to $10,000.00 from their IRA without a penalty fee. Consult a CPA for more information. Having a separate account for your down payment savings prevents you from accidentally confusing the money with your regular spending money, and it is a good way to track your progress.

Saving money will be easier if you have goals in mind. Set realistic weekly, biweekly, or monthly savings goals, and stick to them. If your workplace offers this option, set up your direct deposit so that a portion of each paycheck automatically goes into the savings account you have set aside for your down payment.

Hold Yourself Accountable Saving money will probably require a lifestyle change, and some habits are difficult to break. For instance, if you are used to going out to eat for lunch five days a week, it will be hard to start trying to pack a lunch every day. Set up a time a few times a month, or even once a week, to sit down and go over your expenditures from the week(s) before. Seeing when and how often you make unnecessary purchases can motivate you to make the changes you need to make. Have a close friend or significant other help hold you accountable, (if you’re buying a home together, you can do this for one another).

Providing incentives for yourself can also be a helpful tactic. Set monthly savings goals, and reward yourself at the end of the month if you meet your goals. If your goal is to save $500.00 in a month, and you reach that goal, reward yourself with a small splurge—go out to dinner with friends, or buy yourself something new. This will encourage you to meet your savings goals, and the splurge will be guilt-free, because you have already met your goal for the month.

Get Creative Although the process of saving for a down payment may seem daunting, it doesn’t have to be a chore. There are lots of fun, creative ways to save money. One idea is to earn extra money on the side. Offer to do some odd jobs, such as babysitting, dog walking, home repairs, or housework for your friends or neighbors. If you’re crafty, open an Etsy store and sell your items online. You might be surprised by how much your woodworking, knitting, graphic design, or other skills are in demand. You can also sell clothes or household goods that you’re not using anymore on sites like Craigslis and eBay, or at your local consignment store.

Another way to get creative about saving is to turn it into a game. Have a competition with a friend or family member who is also trying to save money, and see who can save the most by a particular deadline. If you’re buying a home with your significant other, compete with one another, and see how much you can save together!

The decision to buy a home is one of the biggest financial decisions you will ever make. It is important to plan and prepare carefully. Saving money for a down payment can be difficult, but it is well worth the challenge. If you’re thinking about buying a home soon, get started by talking to one of our licensed Mortgage Loan Originators today.

Purchasing a house can be a very exciting step in a person’s life. It requires emotional and financial readiness. In addition to being committed to paying a mortgage every month with varying taxes and fees, most home buyers have to pay a down payment for a house before securing a loan. The average amount that a buyer has to put down is roughly 20% of the purchase price of the home—this depends on the loan product. Saving this much money can seem like an overwhelming feat—here are some tips for you to make this process easier:

1. Determine How Much You can Afford to Spend on a House.

Before starting the process of saving up for a home, figure out how much you are able to afford. Start by looking at your monthly income, and factor in your monthly expenses. Try using an affordable house calculator like the one on our site. Once you know how much you can spend on a house, you can determine how much you need to save for a down payment. In most cases, you will need to save between 5-20% of the sale price for the down payment, but this is based off the loan product you select. Always talk to a Loan Originator for specific down payment information.

2. Set up a Timeline

Let’s say that you have determined that you can pay $200,000 for a house and you want to save up for a 20% down payment. This means you will have to save $40,000 total. This large amount and you shouldn’t expect to save this amount in a short amount of time. You may want to give yourself at least a few years to save this amount. For instance, if you give yourself five years to save the money, you will only have to save $8,000 per year. This number is a lot easier to imagine saving as opposed to $40,000 all at once.

3. Create a Clear Budget

Decide what you can afford to put aside each month. Start by reducing luxury expenses, for example large vacations, dining out every weekend, ect. You might have a family of four and go on vacation during the summer for a week, which could cost $4,000—this could be a substantial contribution to your down payment. If you eliminate eating out one night per week, you could save around $2,600 during the year (if the meal and drinks are around $50).

Try to reduce your essential expenses. Choosing not to buy groceries isn’t a good idea—but managing how much you spend in this area will be very helpful. By reducing the amount you spend on groceries by $20 per week, you could save $1,040 in a year! If you must buy a new car, purchase a car a few thousand dollars under your original maximum price.

Come up with a number that you can comfortably save every month—if you end up with extra money to contribute to this down payment that’s even better.

4. Open up a Separate Savings Account

One of the keys to saving is separating your money from your checking account or other savings accounts. If possible, set up an automatic transfer so your money automatically goes into this account every month. Make sure it is clear to you and your partner that this money is off limits under any circumstances. If you need money for emergencies, create an emergency fund.

5. Put Tax Refunds and End of the Year Bonuses in Your Savings Account.

Whenever you get a large amount of money, try to put all of it or at least half of it into this savings account.

6. Consider Downsizing

If you are currently renting a house or apartment that is too expensive, try switching to a less pricey one when your lease is over.

Don’t be afraid to extend your timeline if necessary. If you follow these tips, you will be well on your way to saving for a down payment. Good luck!

If you are in the market for a new home, one of the first things you should consider financially is how much of a down payment you can make. Most home buyers know that the most common mortgage loan (a Conventional loan) requires 20% down payment. This means that if you purchase a home worth $200,000, you must have $40,000 cash available, on top of the closing costs needed to purchase the home. This may deter many potential home buyers from purchasing because they only have a small amount of money saved. However, Conventional loans are only one of the many loan options available. Here are five of the most widely used mortgage loans and their down payment requirements.

If you are in the market for a new home, one of the first things you should consider financially is how much of a down payment you can make. Most home buyers know that the most common mortgage loan (a Conventional loan) requires 20% down payment. This means that if you purchase a home worth $200,000, you must have $40,000 cash available, on top of the closing costs needed to purchase the home. This may deter many potential home buyers from purchasing because they only have a small amount of money saved. However, Conventional loans are only one of the many loan options available. Here are five of the most widely used mortgage loans and their down payment requirements.