Getting ready to buy a home requires setting a few ducks in a row. For example, ensuring your credit is in the best possible standing. This might require some time (and patience) but it needs to be done. The better your credit score is, the higher the possibility that you will be approved for a loan, as well as receive a better interest rate. The following are ways you can avoid running into common credit issues.

Incorrect Information: It is recommended to obtain your credit report every year, so you can review your information. When you receive it, ensure your name is spelled correctly. If this is inaccurate, there could be data on your report from someone else with the same name. Likewise, double-check all your information, including your address, birthday, employer data and Social Security number. If you do find an error in your credit report, write, don’t email or call, the credit reporting company. While the three credit reporting companies, Equifax, Experian, and TransUnion, offer the option to dispute errors online or by phone, most experts recommend mailing a certified letter, so you have documentation in case your dispute isn’t resolved. In the letter, you should explain what the error is, include photocopies of any documents that support your claim, and ask them to correct the error. You can also include a copy of your report with the error highlighted. Make sure to keep copies of your letter and all documents. Lastly, keep in mind that through the three credit bureaus you are entitled to a free report every year. Therefore, you should request a free credit report from one bureau each quarter to monitor your credit score.

Identity Theft: Identity theft occurs when someone uses your name, Social Security number, date of birth, or other identifying information, without your permission to commit fraud. There are several steps you can take to protect your credit and identity. These are just a few:

Missed or Late Payments: Everyone can be a little forgetful, so if you find you’re having a hard time remembering to make credit card payments, this could affect your credit score. Making credit card payments on time is the fastest way you can enhance your FICO score. If you miss any payments, you will see your score drop rapidly. If you have trouble remembering to make payments, try setting up a calendar reminder on your computer/social device. Every little reminder will help. You might also want to consider setting up automatic payments but be careful not to overdraw your account.

Overspending: Using a credit card is a fast and easy payment method, but if you are not cautious, you could sink into debt before long. It is important to recognize that credit is not free money and must be paid back. Your credit score will reflect the negative impact of having a lot of unpaid debt. The best way to avoid this situation is to curb your spending as much as possible. You don’t want to completely stop using your credit card, but if you create a budget, have a little self-control, and can afford to make larger payments towards your debt, you can improve the state of your credit.

Closing Old Credit Card Accounts: Closing old accounts can lower your credit score. Account history is an important factor of your credit score. Your mortgage lender will be able to see your financial responsibility throughout time, so the older the account is the better. Even if you pay off a credit card, you’re usually better off keeping that card open.

New Accounts: While you are trying to repair your credit score, don’t open any new credit card accounts or make any large purchases. It is best to focus on the accounts you have. It may be tempting to open a new department store credit card to receive a discount, but it may impact your credit negatively if you can’t afford to make the payments. If you really believe you should get one of these credit cards, review your financial plan and determine if you can truly manage the cost.

Achieving your dream of homeownership is possible, it just might take a bit of time and effort. Having good credit will make that dream more financially attainable.

If you have any questions about credit, mortgages, or the homebuying process, contact one of our licensed Mortgage Loan Originators. If you are ready to begin the process, click here to get started!

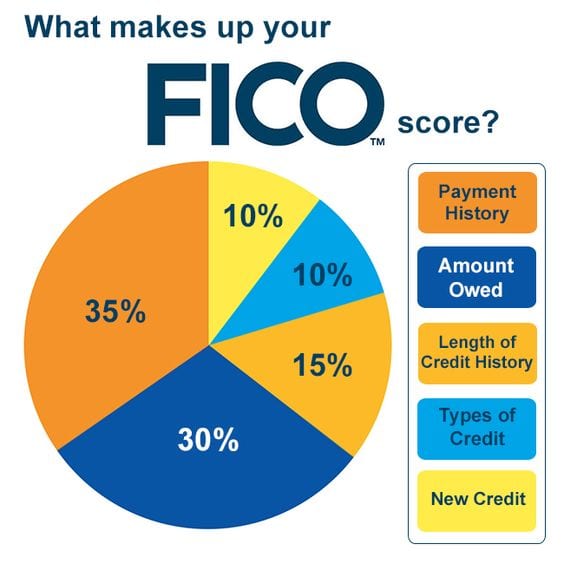

Your credit score is the numerical value assigned based on the information on your credit report. Credit-reporting bureaus use complex and proprietary algorithms to calculate these, but the most widely used are FICO scores. FICO scores can range from 300 to 850, and they give potential lenders an idea of how much of a financial risk you are. To them, the higher the score, the more likely you are to repay the debt and not be late on payments or go into default.

How Are Credit Scores Calculated

Each type of credit score uses algorithms to calculate the potential risk by adding value to items such as payment history and number of credit inquiries. For FICO scores, there are 5 factors used to calculate credit scores. Each factor has different weight in how much they affect your credit score.

Knowing your FICO score and credit worthiness is important, especially if you are looking to get a new loan. You can use websites that provide free credit scores, but often these websites provide you with an estimate rather than your actual score. The Consumer Financial Protection Bureau (CFPB) published a report on the differences between credit scores available to consumers and those to lenders, so make sure you do your research before you submit an application for a loan. Should you have any questions about credit scores, whether you qualify for a mortgage loan with your current credit score, or how to apply for a loan, click here to contact one of our licensed mortgage loan originators today!