When you think about branding yourself as a real estate agent on social media, Google Plus may not be the first social network that comes to mind. If you have a successful Facebook page or Twitter account, then another social media account might not seem necessary; however, Google Plus offers its users many perks that can benefit you and increase your online visibility. Here are four Google Plus tips to help improve your branding and online reach.

Search Engine Optimization

Google automatically ranks posts from a Google Plus page higher than it would rank a business page from another social networking site. When you post links, videos, or photos to your Google Plus page, those posts will show up as top results in Google searches. This means that if a potential client is searching online for information, and your posts are relevant to their search, then your posts and profile will be some of the first results they see.

Communities

Google Plus is full of communities that you can join to meet other industry professionals, network, share news, promote your website, or ask questions. Join communities related to real estate and post your own blogs, or links to your website. This is a great way to build an audience for your content. You can also engage with community members in other ways, such as commenting on their posts, or posting questions for them to answer.

Analytics Your time is valuable. Google business page analytics allows you to save time by posting content that is relevant to your specific audience. Analytics show you the traffic to your page: how many visitors are viewing your page, which posts are more popular than others, how many new visitors you have versus how many are returning visitors, and more. This allows you to tailor your content to suit your audience and learn more about your followers. For example, if you see that your posts about home renovation aren’t driving much engagement, but your posts about home buying are, you know to post more articles about home buying in the future.

Drive Website Traffic You can also use Google Plus to drive business to your website. Share your link and invite your followers to check out your blog posts, customer reviews, online applications, or anything else you want to share. Post it to your main page, then share it to the different communities you belong to. Not only will you reach a wider audience, but these posts will be highly ranked in Google searches, driving more search traffic to your website. Google Plus is a highly valuable tool for real estate professionals. In this competitive industry, online presence and branding are essential. Using Google Plus business pages can improve your online visibility, help you educate potential clients more effectively, and build relationships with other industry professionals. Click here for more information about Google Plus.

LINTHICUM, MD, July 31, 2015— NFM Lending is proud to announce that it was ranked #4 of 50 Best Companies to Work For by Mortgage Executive Magazine. This is the second year in a row that NFM Lending has been recognized as one of the 50 Best Companies to Work For.

Mortgage Executive Magazine conducted an extensive online survey of more than 10,000 Mortgage Loan Originators (MLOs) from over 200 mortgage companies and banks. The survey was limited to licensed MLOs who were presently employed by the companies they were rating. The survey asked participants to rate the company’s culture, loan processing, underwriting, compensation, management, marketing, and technology. The winning selections were based on total MLO votes and average rating score. NFM Lending was ranked #4 of 50 based on average score given by employees.

“Of all the awards, the Best Companies to Work For award means by far the most to me,” said David Silverman, founder and CEO of NFM Lending. “It’s not about numbers or profitability; rather, it’s about how we treat each other and what we stand for as a company. It’s one thing to feel you have a great culture, but when you continue to have your fellow employees vote over and over that they love where they work…that’s real!”

NFM Lending prides itself on its exceptional culture. The company has an open door policy which allows an open line of communication between management and staff. Employees are encouraged to voice their questions and concerns directly to management, so that they can be addressed promptly and correctly. In addition to a competitive salary and a comprehensive benefits package, NFM Lending loan originators receive ongoing support and assistance from qualified support and operations staff, paid time off, and opportunities for trips and giveaways.

In addition to this most recent award, NFM Lending has been recognized many times in the last few years for its exceptional company culture. It was named one of the Washington Post’s Top Work Places in the Washington, D.C. area in 2015; a 2015 Top Mortgage Employer by National Mortgage Professional Magazine; and a Top Work Place in the Baltimore area by The Baltimore Sun in 2012, 2013, and 2014. NFM Lending is proud of all the work its team does to make it a great company to work for.

NFM Lending is a mortgage lending company currently licensed in 29 states in the U.S. The company was founded in Baltimore, Maryland in 1998. They attribute their success in the mortgage industry to their steadfast commitment to customers and the community. NFM Lending has firmly planted itself in the home loan marketplace as “America’s Common Sense Residential Mortgage Lender.”

The new Loan Estimate and Closing Disclosure documents will replace the Good Faith Estimate, the HUD-1, and the Truth in Lending Statement on most residential loan transactions. This change is anticipated to have wide-reaching effects on the mortgage and real estate industries.

The TRID changes were originally scheduled to take place August 1, 2015; however, after pressure from Congress and industry groups to delay this deadline, or to provide a grace period, the CFPB issued a proposal to move this date to October 3, 2015. The proposal was open for public comment on the CFPB website until July 7, 2015. In their press release announcing the delay, the CFPB stated that it believes scheduling the effective date on a weekend will “facilitate implementation by giving industry time over the weekend to launch new systems configurations and to test systems.”

NFM Lending is continuing to prepare its employees and clients for TRID. For more information about this new rule, and what NFM Lending is doing to prepare, click here.

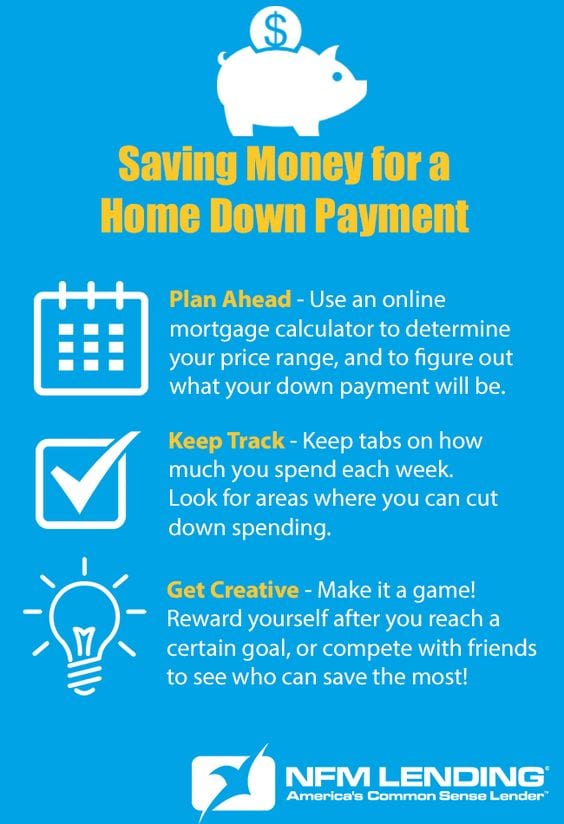

Like any major purchase, a home purchase will require you to put down a certain percentage of the total price as a down payment. The bigger the down payment, the less you will borrow from the mortgage company or bank, and the less your payments will be. With every day expenses and current bills, it can be difficult to find money to begin saving for a down payment. By planning ahead and getting creative, you can begin to save up for a down payment for the mortgage loan that best suits your needs. Here are three ways to save for a down payment and help come up with the savings you need to land the house of your dreams.

Planning Ahead

Saving money for a down payment may take a while, so it helps to have a plan. Start by researching what kind of home you are looking to buy, and the average price of those homes in the area. Then, use an online mortgage calculator to find out what kind of down payment options are best for you, based on your price range. For example, if the homes in the neighborhood you are looking to buy average at $200,000, the standard 20% down payment will be $40,000. Remember, there are loans available with lower down payment options, such as 10% and as low as 3.5%. Talk to your Loan Originator to find out which loan option is right for you.

Once you determine your down payment goals, open a separate savings account. If you’re a first-time home buyer, you can open an investment retirement account (IRA). An IRA will accumulate interest, and first-time home buyers can withdraw up to $10,000.00 from their IRA without a penalty fee. Consult a CPA for more information. Having a separate account for your down payment savings prevents you from accidentally confusing the money with your regular spending money, and it is a good way to track your progress.

Saving money will be easier if you have goals in mind. Set realistic weekly, biweekly, or monthly savings goals, and stick to them. If your workplace offers this option, set up your direct deposit so that a portion of each paycheck automatically goes into the savings account you have set aside for your down payment.

Hold Yourself Accountable Saving money will probably require a lifestyle change, and some habits are difficult to break. For instance, if you are used to going out to eat for lunch five days a week, it will be hard to start trying to pack a lunch every day. Set up a time a few times a month, or even once a week, to sit down and go over your expenditures from the week(s) before. Seeing when and how often you make unnecessary purchases can motivate you to make the changes you need to make. Have a close friend or significant other help hold you accountable, (if you’re buying a home together, you can do this for one another).

Providing incentives for yourself can also be a helpful tactic. Set monthly savings goals, and reward yourself at the end of the month if you meet your goals. If your goal is to save $500.00 in a month, and you reach that goal, reward yourself with a small splurge—go out to dinner with friends, or buy yourself something new. This will encourage you to meet your savings goals, and the splurge will be guilt-free, because you have already met your goal for the month.

Get Creative Although the process of saving for a down payment may seem daunting, it doesn’t have to be a chore. There are lots of fun, creative ways to save money. One idea is to earn extra money on the side. Offer to do some odd jobs, such as babysitting, dog walking, home repairs, or housework for your friends or neighbors. If you’re crafty, open an Etsy store and sell your items online. You might be surprised by how much your woodworking, knitting, graphic design, or other skills are in demand. You can also sell clothes or household goods that you’re not using anymore on sites like Craigslis and eBay, or at your local consignment store.

Another way to get creative about saving is to turn it into a game. Have a competition with a friend or family member who is also trying to save money, and see who can save the most by a particular deadline. If you’re buying a home with your significant other, compete with one another, and see how much you can save together!

The decision to buy a home is one of the biggest financial decisions you will ever make. It is important to plan and prepare carefully. Saving money for a down payment can be difficult, but it is well worth the challenge. If you’re thinking about buying a home soon, get started by talking to one of our licensed Mortgage Loan Originators today.

Stobbe was invited to speak at the expo as a recognized expert in the mortgage industry. She will deliver two seminars at the expo, the first titled “3 Massive Mortgage Money Mistakes to Avoid” and “Why Shopping for the Best Interest Rate can cost you Money”; the second titled “7 Massive Mortgage Mistakes to Avoid” and “VA, FHA & Conventional Financing Highlights.”

“I am thrilled to be a part of the FL Times Union Home Buyer’s Expo!” said Stobbe. “An educated consumer is our best client. I consider it a professional responsibility and I am passionate about empowering home buyers to understand the details about how their mortgage affects their home buying options. I am proud to help raise the standard in mortgage lending by giving home buyers the tools and questions to ask when shopping for a mortgage. I hope that my new book, How to Get Approved for the Best Mortgage Without Sticking a Fork in Your Eye, helps home buyers make smarter decisions with their loan options.”

The Home Buyers Expo will take place from 9:00 a.m. to 3:30 p.m. at the University of North Florida (UNF) University Center. The event is expected to draw attendance from more than 1,500 prospective home buyers and sellers. It will feature speakers on various industry topics, as well as informational booths hosted by real estate agents, builders, mortgage companies, home improvement vendors, and more.

For more information about sponsorship or attendance, call (904)-359-4024. To contact Elysia Stobbe, call her at (904) 446-9007 or visit her website: www.nfmlending.com/estobbe.

About NFM Lending

NFM Lending is a mortgage lending company currently licensed in 29 states across the United States. The company was founded in Baltimore, Maryland in 1998. They attribute their success in the mortgage industry to their steadfast commitment to their customers and their community. NFM Lending has firmly planted itself in the home loan marketplace as “America’s Common Sense Residential Mortgage Lender.”

For more information about NFM Lending, please contact:

LINTHICUM, MD, June 26, 2015 — Elysia Stobbe, a NFM Lending Branch Manager in Jacksonville, FL, released her book, How to Get Approved for the Best Mortgage Without Sticking a Fork in Your Eye, on June 26, 2015.

The book walks potential home buyers through the steps of applying for a home loan: from types of loans, to choosing a mortgage professional, the application process, fees and paperwork, mortgage insurance, and more. Stobbe believes there is a plethora of confusion and misunderstanding among first time homebuyers about loan programs and choosing a mortgage lender. She wrote this book using her expertise to help home buyers understand their options, and navigate the mortgage process successfully.

“My commitment to client service has driven my passion for the individual personal experience in the mortgage industry, and how the regulations and requirements affect real people in real time,” said Stobbe. “With this book I’m privileged and excited to share my knowledge and experience. After reading this book, you will have an understanding of the requirements of the lenders that loan money to home buyers, what loan options you have, and how to navigate government regulations and requirements to your advantage.”

Stobbe has over 12 years of experience in the mortgage industry, and has closed over $250 million in residential mortgage loans. She has been interviewed by the Wall Street Journal and the Washington Post about her mortgage lending expertise. Stobbe has also been ranked a Top Lender in Northeast Florida by Jacksonville Business Journal three years in a row, and recognized as a 2014 Top 50 Business Influencer by Advantage Magazine.

To purchase How to Get Approved for the Best Mortgage Without Sticking a Fork in Your Eye, click here. To contact Stobbe directly, visit her website at www.nfmlending.com/estobbe, contact her at 904-446-9007 or email her at estobbe@nfmlending.com.

About NFM Lending

NFM Lending is a mortgage lending company currently licensed in 29 states in the U.S. The company was founded in Baltimore, Maryland in 1998. They attribute their success in the mortgage industry to their steadfast commitment to customers and the community. NFM Lending has firmly planted itself in the home loan marketplace as “America’s Common Sense Residential Mortgage Lender.™” For more information about NFM Lending, visit www.nfmlending.com, like our Facebook page, or follow us on Twitter.

On Thursday, June 25, 2015, the U.S. Supreme Court ruled in favor of a civil rights group, determining that lending, zoning, sales, or rental practices would be considered discrimination if proven to have a disparate impact on racial minorities, whether that impact was intentional or not.

The 5-4 decision was the result of a case in which a Texas nonprofit, Inclusive Communities Project, Inc., sued the Texas Department of Housing for disproportionately awarding low-income housing tax credits to developers with properties in poor, minority dominated neighborhoods. The Inclusive Communities Project is an organization that seeks to place low-income tenants in wealthier Texas suburbs.

The case hinged on whether the Fair Housing Act allows for disparate impact claims. In a disparate impact claim, the plaintiff must only show evidence of the discriminatory effect of a practice, regardless of whether discriminatory intent was present. The Obama Administration issued new Housing and Urban Development Department rules in 2013 stating that the Fair Housing Act’s definition of discrimination covers disparate-impact situations.

This decision is expected to have wide-reaching effects on the lending, insurance, and other industries. More information about the Fair Housing Act can be found here. To read the full Supreme Court decision, click here.

LINTHICUM, MD, June 19, 2015 — NFM Lending is pleased to announce that it has been ranked a 2015 Top Workplace in the Washington, D.C. area by the Washington Post.

NFM Lending received the award at a ceremony held on Thursday, June 18, 2015. Since its founding in 1998, NFM Lending has grown from a small mortgage brokerage to a lender with retail branches throughout the United States; the company has locations in 29 states, with 7 locations in the D.C. area, including its corporate headquarters. NFM prides itself on its company culture.

“This event is an additional confirmation that the culture of NFM Lending is one that promotes hard work in a healthy work environment,” said LaTasha Rowe, General Counsel at NFM. “As an executive it is easy to say that this is a great company to work for. But my opinion really doesn’t matter if our employees don’t believe it as well. Tonight begins the work NFM Lending must do to improve our ranking next year. Congratulations to our stellar staff!”

Each year, the Washington Post distributes a survey to the employees of Washington, D.C. area companies, asking them to evaluate their workplaces. The survey asks participants to rank their companies on quality of leadership, work-life balance, pay and benefits, and more. This year, NFM Lending was among 150 small, midsized, and large companies that made the final cut for inclusion on the Top Workplace list.

NFM Lending was also named a 2015 Top Mortgage Employer by National Mortgage Professional Magazine earlier this year, and a Top Workplace by The Baltimore Sun in 2012, 2013, and 2014. NFM Lending is proud of these accomplishments, and the work its team does to make it a Top Workplace.

About NFM Lending

NFM Lending is a mortgage lending company currently licensed in 29 states across the United States. The company was founded in Baltimore, Maryland in 1998. They attribute their success in the mortgage industry to their steadfast commitment to their customers and their community. NFM Lending has firmly planted itself in the home loan marketplace as “America’s Common Sense Residential Mortgage Lender.”

For more information about NFM Lending, please contact:

LINTHICUM, MD, June 18, 2015 — The Consumer Financial Protection Bureau (CFPB) announced Wednesday, June 17, 2015, that implementation of the new TILA-RESPA Integrated Disclosures (TRID), which will replace the Good Faith Estimate, the HUD-1, and the Truth in Lending Statement, may be delayed from August 1 until October 1, 2015.

Richard Cordray, Director of the CFPB, said that the delayed deadline was implemented to correct an administrative error. Cordray’s full statement, published on the CFPB website, is below:

“The CFPB will be issuing a proposed amendment to delay the effective date of the Know Before You Owe rule until October 1, 2015. We made this decision to correct an administrative error that we just discovered in meeting the requirements under federal law, which would have delayed the effective date of the rule by two weeks. We further believe that the additional time included in the proposed effective date would better accommodate the interests of the many consumers and providers whose families will be busy with the transition to the new school year at that time.”

NFM Lending will continue to prepare its employees and clients for TRID. For more information about what NFM Lending is doing to prepare for these important changes, visit www.nfmlending.com/ready-for-TRID.

About NFM Lending

NFM Lending is a mortgage lending company currently licensed in 29 states across the United States. The company was founded in Baltimore, Maryland in 1998. They attribute their success in the mortgage industry to their steadfast commitment to their customers and their community. NFM Lending has firmly planted itself in the home loan marketplace as “America’s Common Sense Residential Mortgage Lender.”

For more information about NFM Lending, please contact:

The Consumer Financial Protection Bureau (CFPB) issued a statement on Wednesday, June 3, 2015, stating that its enforcement of the TILA-RESPA INTEGRATED DISCLOSURES (“TRID”) will be sensitive to mortgage lenders making a good faith effort to enforce the new rule. Richard Cordray, Director of the CFPB, addressed the statement to Senators Joe Donnelly and Tim Scott, and recognized that the implementation of TRID will post challenges to industry professionals. Cordray also outlined the CFPB’s plan for implementing the new rule.

Cordray was also adamant that TRID would not delay most closings, and clarified the three circumstances under which an additional 3-day review period, or re-disclosure, will be required:

An APR increase of more than 1/8 of a percent for fixed-rate loans, or 1/4 of a percent for adjustable loans. A decrease in APR will not require re-disclosure, if it is based on changes to interest rate or other fees.

The addition of a prepayment penalty

The loan product itself changes, (i.e., from fixed-rate to adjustable-rate)

Cordray closed his statement by saying that the CFPB’s support of the implementation of TRID will not end on August 1, and that regulators will be sensitive to lenders making good-faith efforts to enforce the new rule. To read the full statement, click here.

While this is a step in the right direction, both Congress and the mortgage industry quickly responded that still more was needed.

“Nearly 300 Senators and House Members have written to Director Cordray asking for a formalized hold harmless,” said U.S. Reps. Blaine Luetkemeyer (R-MO) and Randy Neugebauer (R-TX) in a joint statement. “Anything short of that is unacceptable.”

Google Plus is a highly valuable tool for real estate professionals. In this competitive industry, online presence and branding are essential. Using Google Plus business pages can improve your online visibility, help you educate potential clients more effectively, and build relationships with other industry professionals. Click here for more information about Google Plus.

Google Plus is a highly valuable tool for real estate professionals. In this competitive industry, online presence and branding are essential. Using Google Plus business pages can improve your online visibility, help you educate potential clients more effectively, and build relationships with other industry professionals. Click here for more information about Google Plus.

LINTHICUM, MD, June 26, 2015 — Elysia Stobbe, a

LINTHICUM, MD, June 26, 2015 — Elysia Stobbe, a  LINTHICUM, MD, June 19, 2015 — NFM Lending is pleased to announce that it has been ranked a 2015 Top Workplace in the Washington, D.C. area by the

LINTHICUM, MD, June 19, 2015 — NFM Lending is pleased to announce that it has been ranked a 2015 Top Workplace in the Washington, D.C. area by the